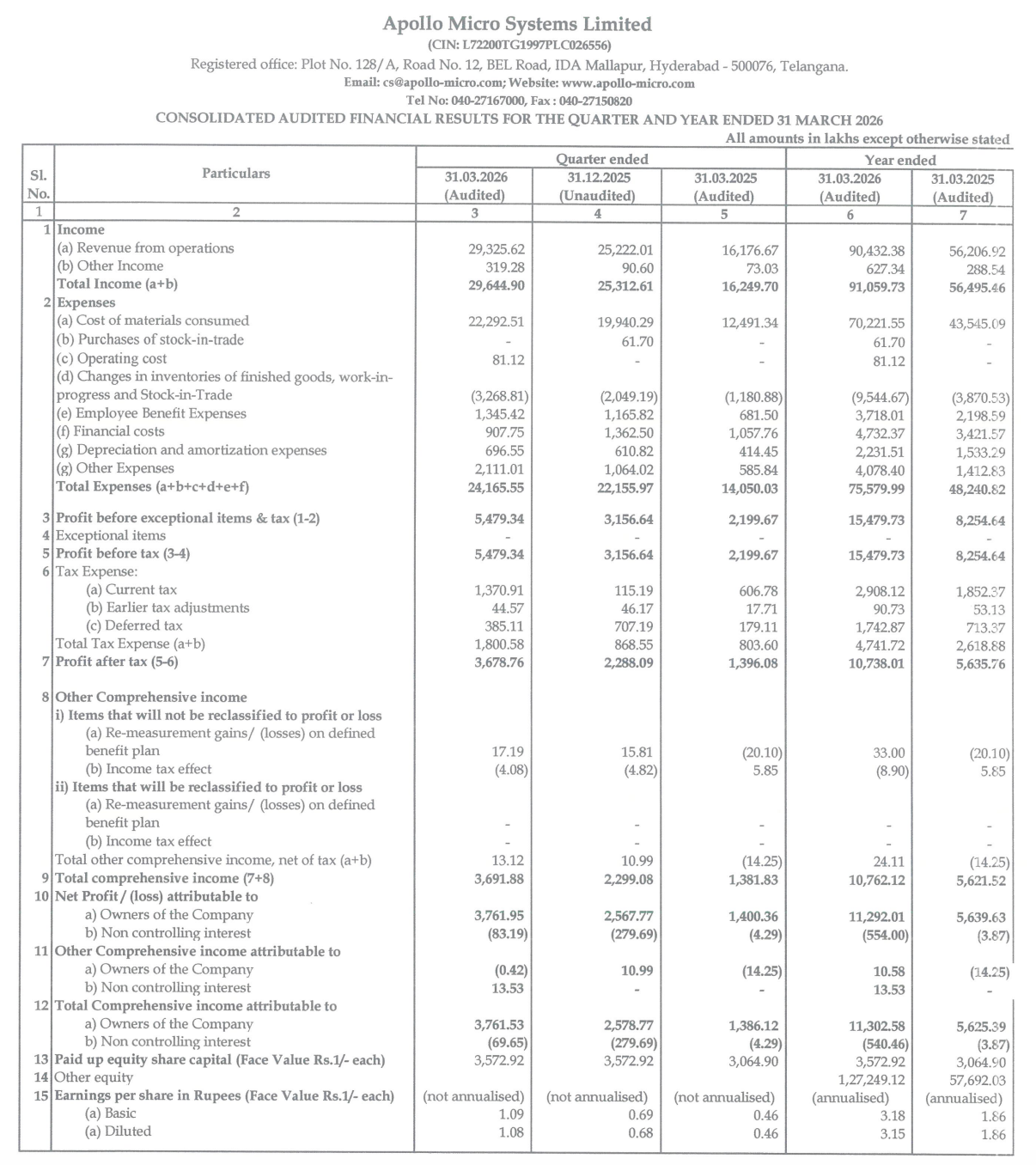

Quarter Ended: March 2026

Apollo Micro Systems Limited – Q4 FY26 Results

NSE

apollo

BSE

540879

Apollo Micro Systems Ltd reported strong Q4 FY26 performance with robust YoY growth in revenue, PBT, and PAT driven by higher execution in defence and electronic systems business.

key financial highlights

- Revenue from Operations:

- Revenue (Q4 FY26): ₹29,325.62 Lakhs

- QoQ Change: +16.27%

- YoY Change: +81.28%

- Previous Quarter (Q3 FY26): ₹25,222.01 Lakhs

- Previous Year (Q4 FY25): ₹16,176.67 Lakhs

- Revenue (Q4 FY26): ₹29,325.62 Lakhs

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹3,678.76 Lakhs

- QoQ Change: +60.78%

- YoY Change: +163.51%

- Previous Quarter (Q3 FY26): ₹2,288.09 Lakhs

- Previous Year (Q4 FY25): ₹1,396.08 Lakhs

- PAT (Q4 FY26): ₹3,678.76 Lakhs

- QoQ Performance:

- Revenue Trend: Revenue improved strongly due to higher execution and operational scale-up.

- Profit Trend: Profitability improved sharply supported by operating leverage and better earnings conversion.

- Revenue Trend: Revenue improved strongly due to higher execution and operational scale-up.

Margin Analysis

Drivers:

- Strong operating leverage improved profitability.

- Cost of materials remained elevated but was absorbed through higher revenue scale.

- Employee and operational expenses increased in line with business expansion.

- Finance costs moderated sequentially compared to Q3 FY26.

Insight:

- The company demonstrated strong scalability with earnings growth significantly outpacing revenue growth.

Earning quality check

Key Drivers:

- Strong rise in receivables and inventories impacted operating cash flow.

- Operating cash flow remained negative despite strong profitability.

- Higher working capital deployment supported business expansion.

Interpretations:

- Reported earnings remain strong, though cash conversion weakened due to aggressive working capital expansion.

balance sheet Analysis

- Total Assets: ₹2,36,850.83 Lakhs

- Total Liabilities: ₹1,06,028.79 Lakhs

Insight:

- The company materially expanded its asset base during FY26 with strong growth in inventories, receivables, CWIP, and goodwill, indicating aggressive expansion and execution ramp-up.

key risks

- Negative operating cash flow due to rising working capital.

- High receivables and inventory levels may impact liquidity.

- Elevated debt levels increase financial obligations.

- Defence order execution timelines remain critical.

management strategy signals

Focus Area:

- Expanding defence electronics manufacturing capabilities.

- Increasing execution of large defence and aerospace orders.

- Capacity expansion through capital expenditure and CWIP investments.

- Strengthening long-term order pipeline.

Financial metrics table

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹29,644.90 Lakhs | +17.08% | +82.43% |

| PBT | ₹5,479.34 Lakhs | +73.59% | +149.10% |

| PAT | ₹3,678.76 Lakhs | +60.78% | +163.51% |

Apollo Micro Systems Ltd delivered an impressive Q4 FY26 performance with strong growth in revenue and profitability supported by robust defence sector execution. The company continues to aggressively expand operations and manufacturing capabilities. However, rising working capital intensity and negative operating cash flow remain important monitorable factors going forward.

Official Exchange Filing: Apollo Microsystems Limited

Quarterly Performance Context

COST OF OPERATIONS AS % OF REVENUE

82%

NET PROFIT AS % OF REVENUE

12%

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED