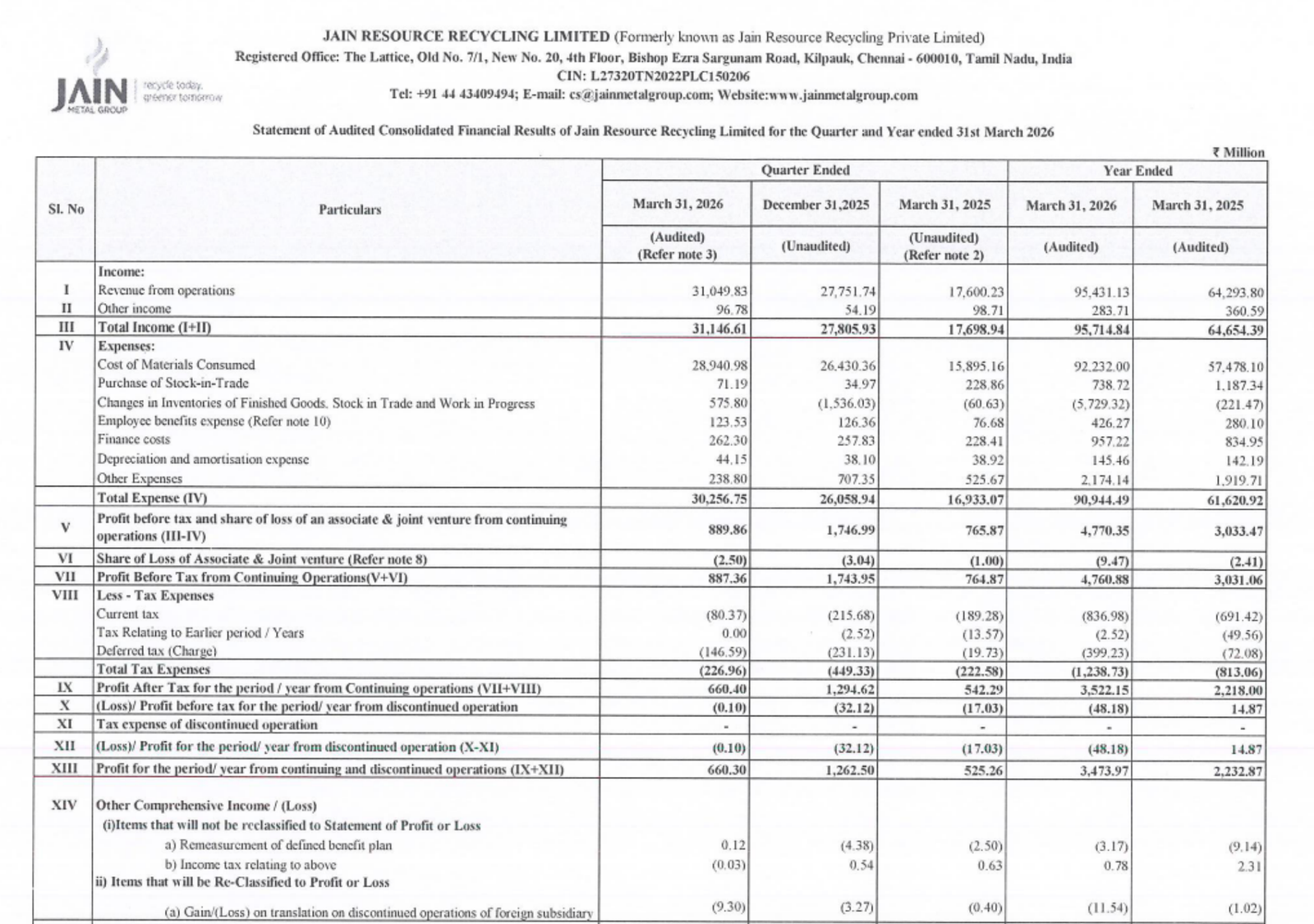

Quarter Ended: March 2026

Jain Resource Recycling Limited – Q4 FY26 Results

NSE

jainrec

BSE

544537

Jain Resource Recycling Ltd reported strong YoY revenue and profit growth in Q4 FY26, although profitability softened sequentially compared to Q3 FY26.

key financial highlights

- Revenue from Operations:

- Revenue (Q4 FY26): ₹31,049.83 Million

- QoQ Change: +11.89%

- YoY Change: +76.42%

- Previous Quarter (Q3 FY26): ₹27,751.74 Million

- Previous Year (Q4 FY25): ₹17,600.23 Million

- Revenue (Q4 FY26): ₹31,049.83 Million

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹660.40 Million

- QoQ Change: -48.99%

- YoY Change:+21.79%

- Previous Quarter (Q3 FY26): ₹1,294.62 Million

- Previous Year (Q4 FY25): ₹542.29 Million

- PAT (Q4 FY26): ₹660.40 Million

- QoQ Performance:

- Revenue Trend: Revenue improved sequentially on higher operational scale and stronger segment contribution.

- Profit Trend: Profit declined sharply QoQ due to increased operating expenses and pressure on margins.

- Revenue Trend: Revenue improved sequentially on higher operational scale and stronger segment contribution.

Margin Analysis

Drivers:

- Raw material consumption remained elevated at ₹28,940.98 Million.

- Finance costs increased to ₹262.30 Million.

- Other expenses rose significantly during the quarter.

- Higher revenue growth partially offset cost pressures.

Insight:

- Revenue momentum remained strong, but margin compression impacted quarterly earnings growth.

Segment performance

Segments: Copper & Copper Ingots

- Revenue: ₹19,445.09 Million

- Insights:

- Largest contributor to consolidated revenue.

- Strong YoY growth versus ₹7,931.27 Million in Q4 FY25.

Segments: Lead & Lead Alloy Ingots

- Revenue: ₹10,457.96 Million

- Insights:

- Delivered solid contribution to revenue and profitability.

- Segment result stood at ₹782.93 Million.

Segments: Aluminium & Aluminium Alloys

- Revenue: ₹1,084.38 Million

- Insights:

- Stable contributor within the diversified recycling portfolio.

- Segment profitability remained positive.

Segment insight

Business Summary:

Copper and lead alloy businesses remained the core growth drivers during Q4 FY26, contributing the majority of consolidated revenue.

Key Characteristics:

- Copper segment dominated overall business mix.

- Lead segment maintained healthy profitability.

- Aluminium segment provided diversification support.

Earning quality check

Key Drivers:

- Strong topline growth supported earnings expansion.

- Finance cost and operational expenses weighed on net profit.

- Working capital intensity remained elevated.

Interpretations:

- Quarterly earnings quality stayed stable operationally, though profit conversion weakened sequentially due to cost escalation.

balance sheet Analysis

- Total Assets: ₹33,822.11 Million

- Total Liabilities: ₹18,240.98 Million

Insight:

- The company significantly expanded its asset base during FY26, supported by higher inventory, receivables, and current assets, while equity strengthened materially.

key risks

- High working capital requirements may pressure liquidity.

- Commodity price volatility can affect margins.

- Rising borrowings and finance costs remain monitorable.

management strategy signals

Focus Area:

- Scaling recycled metal operations.

- Expanding copper and lead alloy business volumes.

- Strengthening operational infrastructure and supply chain.

Financial metrics table

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Revenue from Operations | ₹31,049.83 Million | +11.89% | +76.42% |

| PBT | ₹887.36 Million | -49.12% | +16.02% |

| PAT | ₹660.40 Million | -48.99% | +21.79% |

Jain Resource Recycling Ltd delivered a strong revenue performance in Q4 FY26 with robust YoY expansion across key business segments. However, rising expenses and finance costs impacted sequential profitability. The company remains in a strong growth phase, but investors should closely monitor margins, working capital, and cash flow trends in upcoming quarters.

Official Exchange Filing: Jain Resources Recycling Limited

Quarterly Performance Context

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED