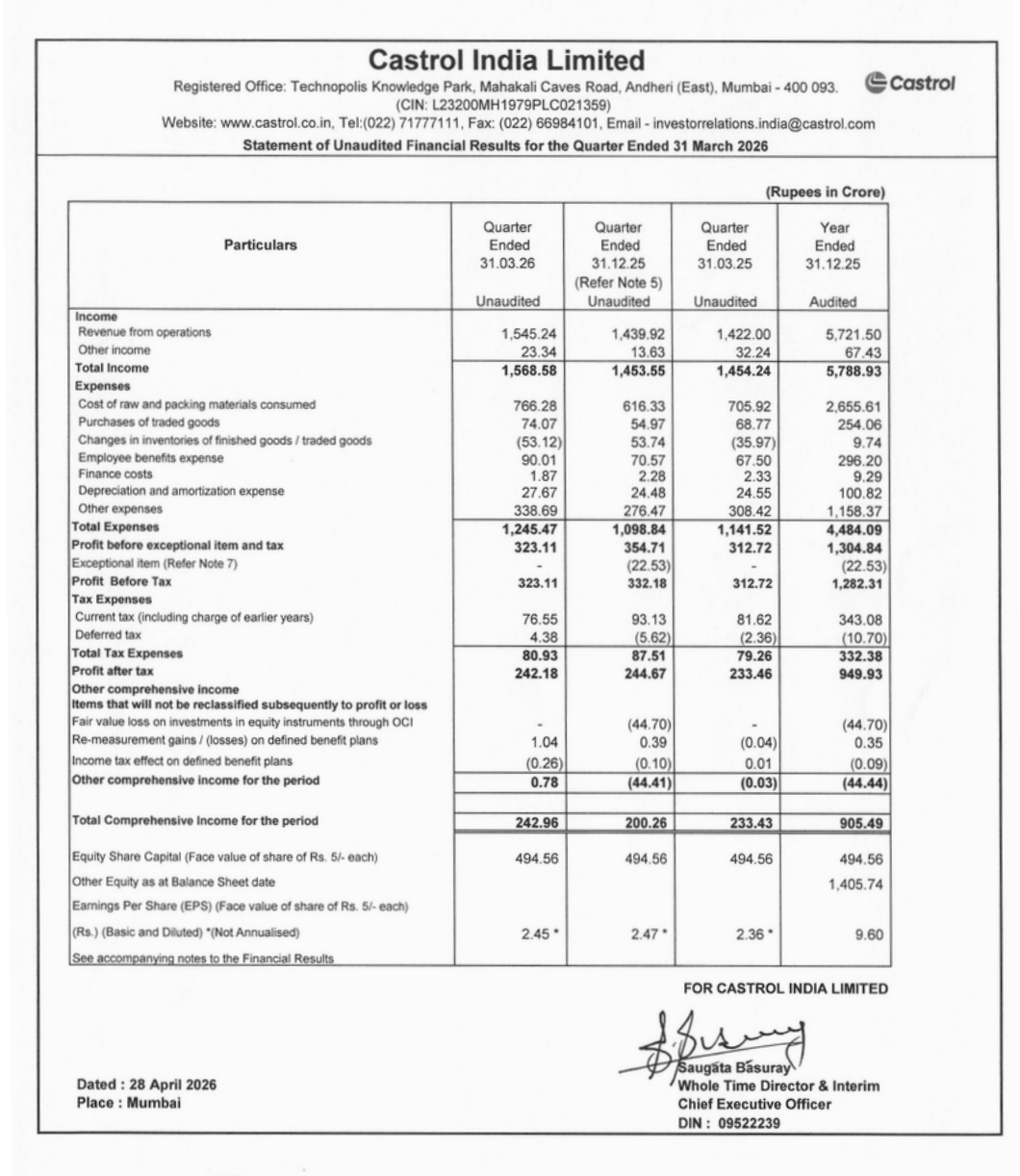

Quarter Ended: March 2026

Castrol India Q1 CY2026 Results Analysis

NSE

castrolind

BSE

500870

Castrol delivered steady growth driven by distribution expansion and strong brand positioning, while maintaining profitability despite rising cost pressures

key financial highlights

- Revenue from Operations:

- Total Income (Q4 FY26): ₹1,545.24 Cr

- QoQ Change: +7.32%

- YoY Change: +8.66%

- Previous Quarter (Q3 FY26): ₹1,439.92 Cr

- Previous Year (Q4 FY25): ₹1,422.00 Cr

- Total Income (Q4 FY26): ₹1,545.24 Cr

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹242.18 Cr

- QoQ Change: -1.02%

- YoY Change: +3.74%

- Previous Quarter (Q3 FY26): ₹244.67 Cr

- Previous Year (Q4 FY25): ₹233.46 Cr

- PAT (Q4 FY26): ₹242.18 Cr

- QoQ Performance

- Revenue Trend: Positive

- Profit Trend: Slightly Flat

Margin Analysis

Key Drivers:

- Increase in raw material and packing costs

- Higher other operating expenses

- Controlled employee and finance costs

- Strong pricing discipline

Key Signal: Margins are stable but slightly under pressure, indicating cost inflation being partially absorbed

Segment insight

Summary:

- Growth driven by distribution expansion, rural penetration, and premium product focus

Characteristics:

- Expansion to ~43,000 rural outlets

- Strong auto service ecosystem (~150,000 outlets)

- Focus on EV and industrial segments

- Increasing digital engagement (FastScan network growth)

Earning quality check

Drivers:

- Strong core operating income

- Minimal reliance on other income

- Stable cash-generating business model

Interpretation:

- Earnings quality is high, driven by consistent operational performance and strong brand moat

balance sheet Analysis

- Total Assets: Not fully disclosed

- Total Liabilities: Not fully disclosed

Insight:

- Asset-light FMCG-like model

- Strong cash generation capability

- Low leverage business structure

key risks

- Raw material price volatility (base oil)

- Currency fluctuations

- Increasing competition in lubricant segment

- EV transition risk (long-term demand shift)

management strategy signals

Focus Area:

- Rural expansion

- Premium product portfolio

- Industrial segment growth

- Digital ecosystem strengthening

- Cost discipline and pricing strategy

Financial Metrics

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹1,568.58 Crore | +7.91% | +7.86% |

| PBT | ₹323.11 Crore | -2.73% | +3.32% |

| PAT | ₹242.18 Crore | -1.02% | +3.74% |

Castrol India continues to demonstrate a resilient and consistent business model, delivering steady growth with strong margins. While cost pressures are emerging, the company’s brand strength, distribution reach, and pricing powerprovide confidence in sustained long-term performance

Official Exchange Filing: Castrol India Ltd

Quarterly Performance Context

COST OF OPERATIONS AS % OF REVENUE

81%

NET PROFIT AS % OF REVENUE

16%

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED