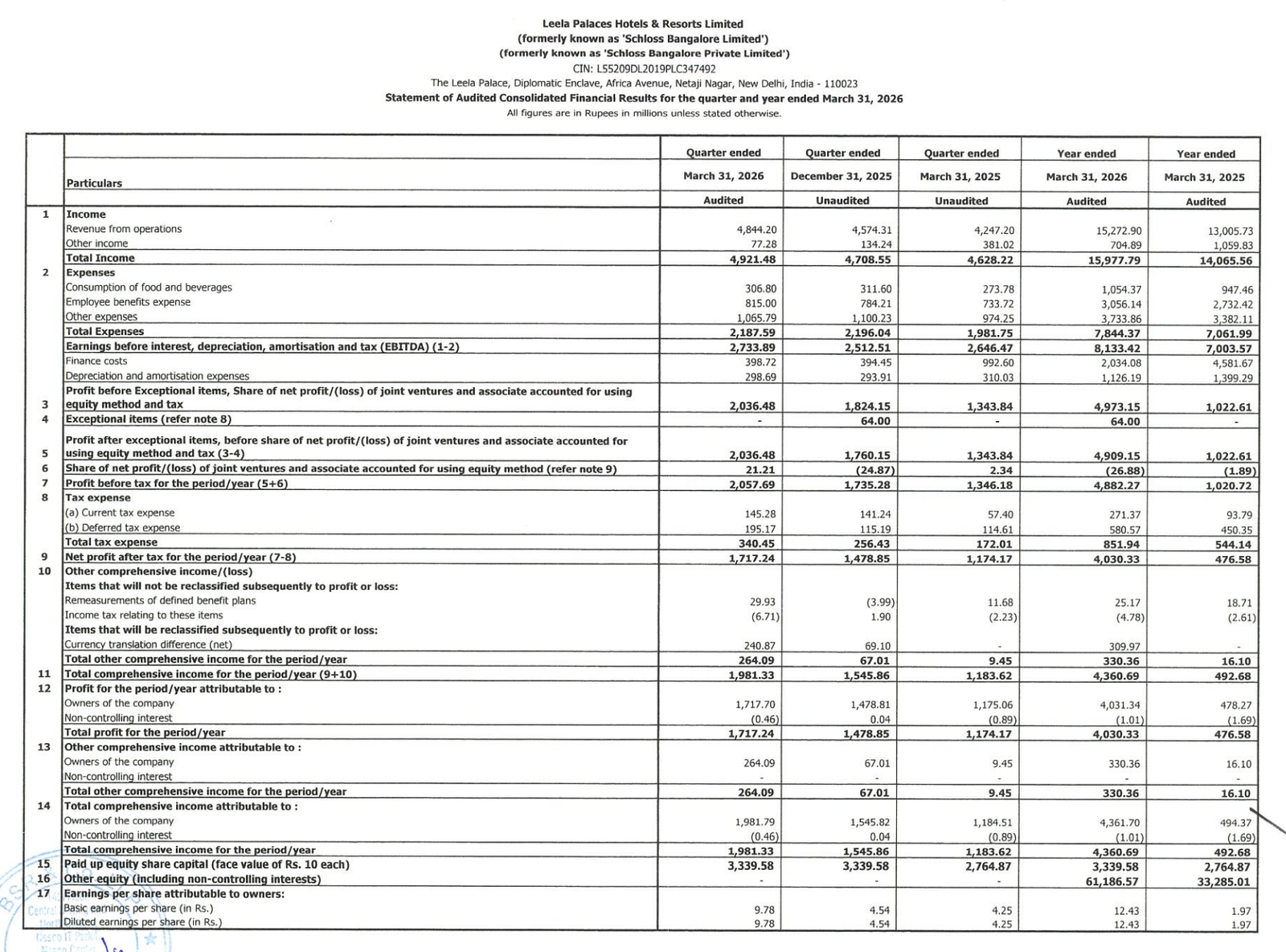

Quarter Ended: March 2026

Leela Palaces Hotels & Resorts – Q4 FY26 Results Analysis

NSE

theleela

BSE

544408

Strong rebound in profitability supported by improved operating performance, reduced finance costs, and balance sheet strengthening

key financial highlights

- Revenue from Operations:

- Revenue (Q4 FY26): ₹4,844.20 Million

- QoQ Change: +5.94%

- YoY Change: +13.99%

- Previous Quarter (Q3 FY26): ₹4,574.31 Million

- Previous Year (Q4 FY25): ₹4,247.20 Million

- Revenue (Q4 FY26): ₹4,844.20 Million

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹1,717.24 Million

- QoQ Change: +16.19%

- YoY Change: +46.28%

- Previous Quarter (Q3 FY26): ₹1478.85 Million

- Previous Year (Q4 FY25): ₹1174.17 Million

- PAT (Q4 FY26): ₹1,717.24 Million

- QoQ Performance

- Revenue Trend: Positive

- Profit Trend: Strong Growth

Margin Analysis

Key Drivers:

- Strong operating leverage in hospitality business

- Significant reduction in finance costs (₹2,034 Mn vs ₹4,581 Mn YoY)

- Stable cost structure despite revenue growth

- Higher premium occupancy / pricing power

Key Signal: Sharp margin expansion, driven by both operational improvement and financial restructuring

Segment insight

Summary:

- Performance driven by premium hospitality demand recovery and pricing strength

Characteristics:

- Strong growth in luxury segment demand

- Improved occupancy and ARRs

- Focus on high-margin properties

Earning quality check

Drivers:

- Core EBITDA strength

- Lower finance cost burden

- Minimal reliance on one-offs

Interpretation:

- Earnings quality is improving significantly, with transition from leveraged stress to stable profitability

balance sheet Analysis

- Total Assets: ₹89,236.84 Mn (~₹8,924 Cr)

- Total Liabilities: ₹24,710.69 Mn (~₹2,471 Cr)

Insight:

- Massive debt reduction (borrowings down sharply YoY)

- Strong increase in equity base (₹64,526 Mn)

- Improved liquidity position

- Transition towards healthier capital structure

key risks

- Cyclicality in hospitality demand

- High dependence on luxury segment

- Exposure to global travel trends

- Cost pressures (energy, staffing)

management strategy signals

Focus Area:

- Premium segment expansion

- Debt reduction

- Operational efficiency

- Enhancing occupancy and ARRs

Financial Metrics

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹492.15 Crore | +4.53% | +6.34% |

| PBT | ₹205.7 Crore | +18.62% | +52.70% |

| PAT | ₹171.7 Crore | +16.19% | +46.28% |

Leela Palaces has delivered a strong turnaround performance, with profitability surging due to operating leverage and a sharp reduction in debt burden. The company is now entering a high-margin growth phase, though sustainability will depend on maintaining premium demand momentum.

Official Exchange Filing: Leela Palaces Hotels & Resorts Ltd

Quarterly Performance Context

COST OF OPERATIONS AS % OF REVENUE

45%

NET PROFIT AS % OF REVENUE

35.45%

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED