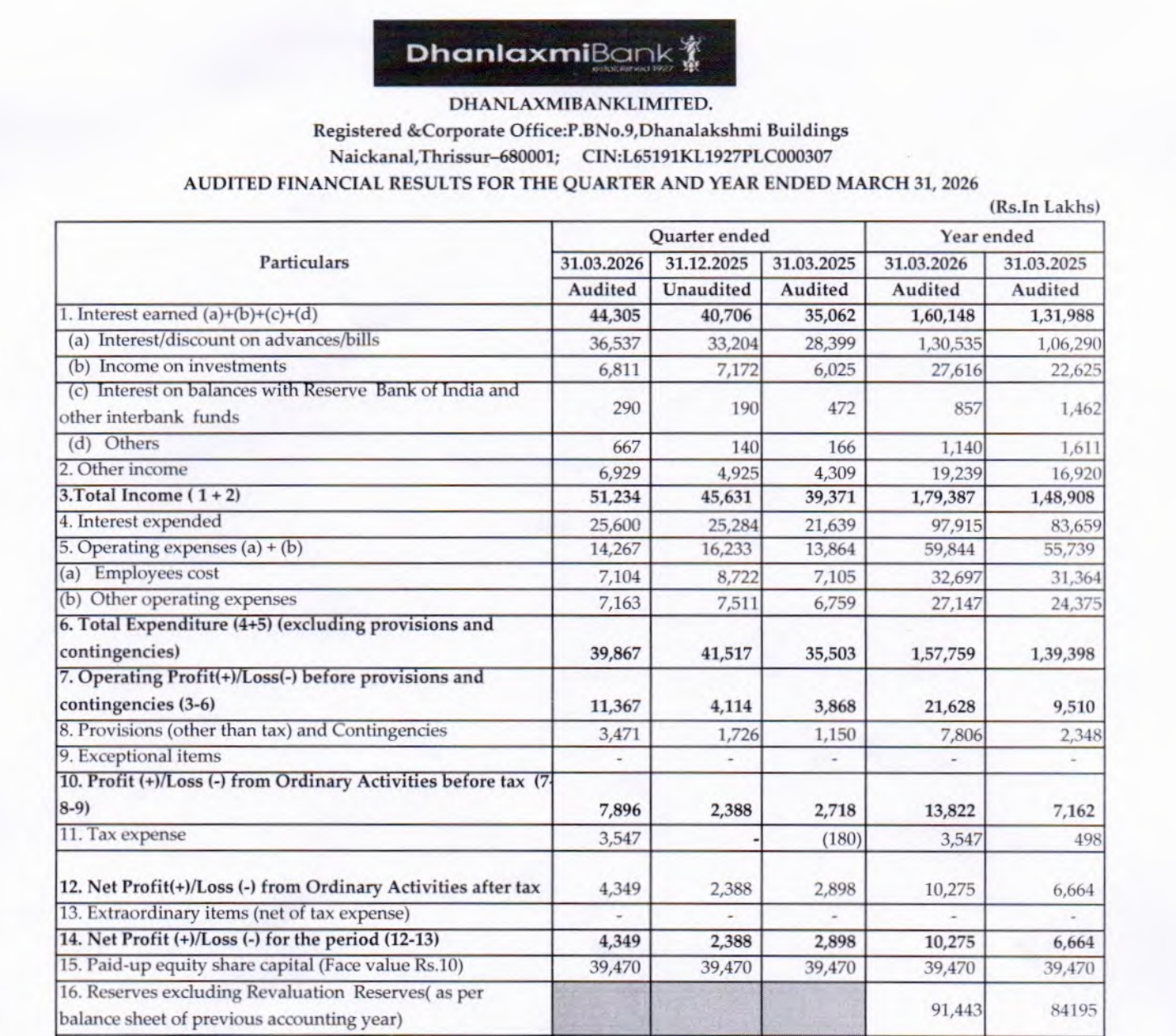

Quarter Ended: March 2026

Dhanlaxmi Bank Q4 FY26 Results Analysis

NSE

dhanbank

BSE

532180

The bank delivered robust profit growth supported by higher interest income, improved operating efficiency, and stable asset quality

key financial highlights

- Revenue from Operations:

- Revenue (Q4 FY26): ₹512.34 Cr

- QoQ Change: +12.31%

- YoY Change: +30.13%

- Previous Quarter (Q3 FY26): ₹456.31 Cr

- Previous Year (Q4 FY25): ₹393.71 Cr

- Revenue (Q4 FY26): ₹512.34 Cr

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹43.49 Cr

- QoQ Change: +82.09%

- YoY Change: +50.07%

- Previous Quarter (Q3 FY26): ₹23.88 Cr

- Previous Year (Q4 FY25): ₹28.98 Cr

- PAT (Q4 FY26): ₹43.49 Cr

- QoQ Performance

- Revenue Trend: Strong Growth

- Profit Trend: Strong Growth

Margin Analysis

Key Drivers:

- Strong growth in interest income (core banking revenue)

- Controlled operating expenses

- Improved operating leverage

- Increase in yield on advances

Key Signal: Margins are expanding sharply, reflecting improved profitability and efficiency

Segment performance

Segment: Treasury

Insights:

- Revenue stable, contributing steady income

- Improved profitability vs last year

Segment: Retail Banking

Insights:

- Strong growth driver

- Significant increase in revenue and profits

Segment: Corporate / Wholesale Banking

Insights:

- Moderate performance

- Still recovering but contributing positively

Segment: Other Banking Operations

Insights:

- Small but stable contribution

Segment insight

Summary:

- Growth is retail-led, supported by improving treasury performance

Characteristics:

- Increasing retail loan focus

- Diversified revenue streams

- Reduced dependence on corporate lending

Earning quality check

Drivers:

- Strong core interest income growth

- Controlled provisions relative to growth

- Limited reliance on one-off gains

Interpretation:

- Earnings quality is improving, with sustainable growth from core banking operations

balance sheet Analysis

- Total Assets: ₹21,237 Cr

- Total Liabilities: ₹19,763 Cr

Insight:

- Strong growth in deposits (~₹18,642 Cr)

- Advances increased significantly (~₹14,918 Cr)

- Stable capital base

- Healthy liquidity position

key risks

- Rising NPAs (absolute level still high)

- Competition in retail banking

- Margin pressure if interest rates soften

- PSU/private bank competition

management strategy signals

Focus Area:

- Retail banking expansion

- CASA growth

- Asset quality improvement

- Cost control

Financial Metrics

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹512.34 Crore | +12.31% | +30.13% |

| PBT | ₹78.96 Crore | +231% | +190% |

| PAT | ₹43.49 Crore | +82.09% | +50.07% |

Dhanlaxmi Bank is showing a clear turnaround with strong earnings momentum, driven by retail growth and improved operating efficiency. While asset quality risks remain, the overall trajectory indicates sustainable recovery and strengthening fundamentals.

Official Exchange Filing: Dhanlaxmi Bank Ltd

Quarterly Performance Context

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED