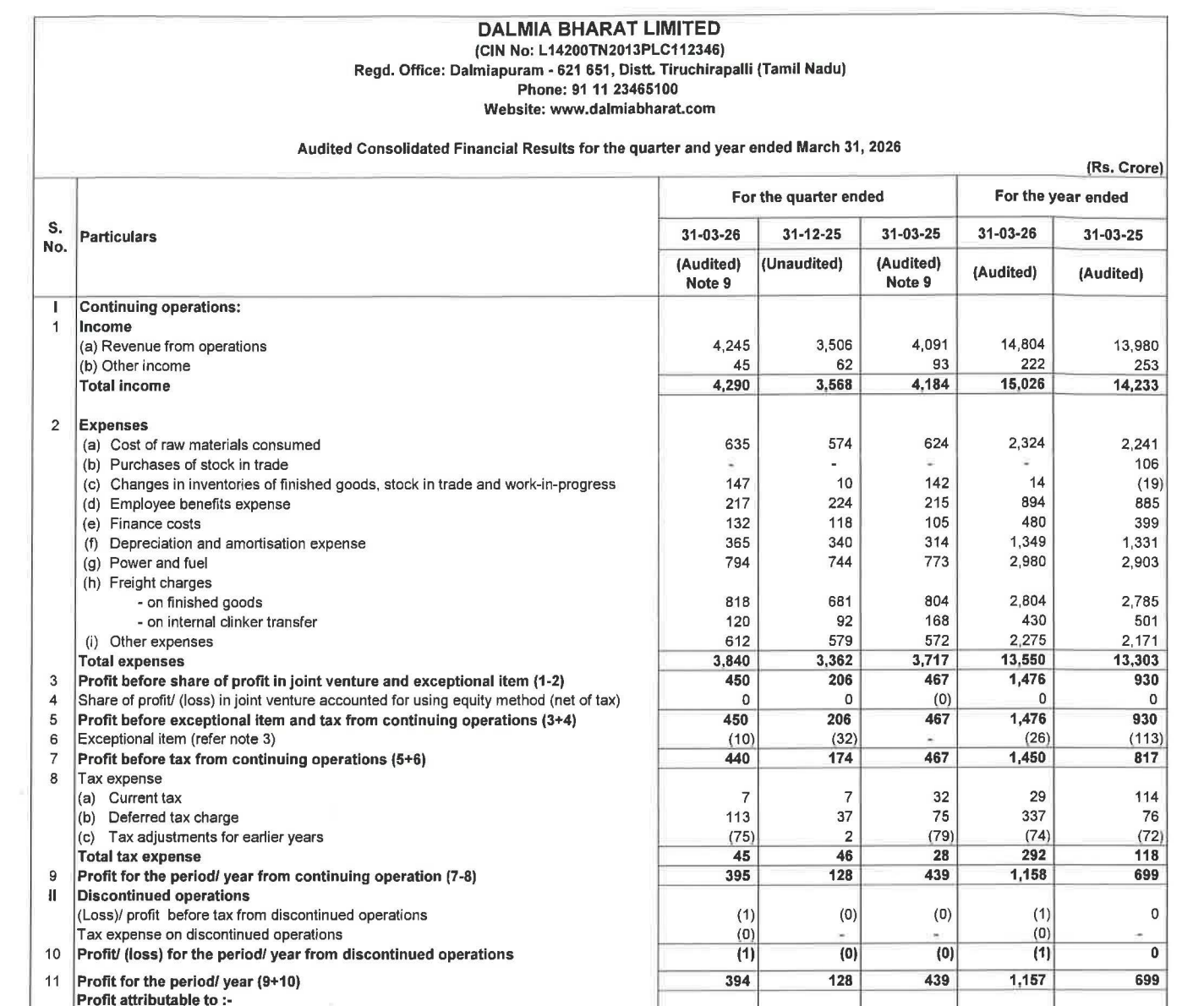

Quarter Ended: March 2026

Dalmia Bharat – Q4 FY26 Results Analysis

NSE

dalbharat

BSE

542216

Strong profitability improvement YoY, but heavy capex, working capital build-up, and rising debt need close monitoring

key financial highlights

- Revenue from Operations:

- Revenue (Q4 FY26): ₹4,290 Cr

- QoQ Change: +20.2%

- YoY Change: +2.5%

- Previous Quarter (Q3 FY26): ₹3,568 Cr

- Previous Year (Q4 FY25): ₹4,184 Cr

- Revenue (Q4 FY26): ₹4,290 Cr

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹394 Cr

- QoQ Change: +207%

- YoY Change: -10.3%

- Previous Quarter (Q3 FY26): ₹128 Cr

- Previous Year (Q4 FY25): ₹439 Cr

- PAT (Q4 FY26): ₹394 Cr

- QoQ Performance

- Revenue Trend: Strong Recovery

- Profit Trend: Sharp Recovery

Margin Analysis

Key Drivers:

- Power & fuel costs remain elevated (₹794 Cr in Q4)

- Freight and logistics costs still high

- Operating leverage kicked in QoQ due to volume recovery

Key Signal: Margins improved sequentially, but YoY pressure persists due to cost structure

Earning quality check

Drivers:

- Strong operating cash flow: ₹2,278 Cr

- Significant depreciation (₹1,349 Cr annually)

- Finance costs elevated (₹480 Cr annually)

- Exceptional items impacting comparability

Interpretation:

- Earnings are operationally supported but capital-intensive nature and high finance costs reduce net profitability efficiency.

balance sheet Analysis

- Total Assets: ₹33,312 Cr

- Total Liabilities: ₹15,189 Cr

Insight:

- Increase in borrowings (₹6,168 Cr vs ₹4,605 Cr YoY)

- Strong asset base driven by capex (PPE ₹16,118 Cr)

- Moderate leverage increase indicates expansion phase

key risks

- Rising fuel and logistics costs

- High capital expenditure leading to leverage increase

- Cyclical nature of cement demand

- Margin compression risk in competitive pricing environment

management strategy signals

Focus Area:

- Capacity expansion

- Cost optimization

- Strengthening operational efficiency

- Improving cash flow generation

Financial Metrics

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹4,290 Crore | +20.2% | +2.5% |

| PBT | ₹440 Crore | +152.9% | -5.8% |

| PAT | ₹394 Crore | +207.8% | -10.3% |

Dalmia Bharat delivered a strong QoQ recovery, but YoY profitability decline and persistent cost pressures remain key concerns. The company is clearly in an expansion cycle, which supports long-term growth but may continue to weigh on margins in the near term.

Official Exchange Filing: Dalmia Bharat Ltd

Quarterly Performance Context

COST OF OPERATIONS AS % OF REVENUE

90%

NET PROFIT AS % OF REVENUE

9.3%

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED