Quarterly Financial Results

Emmvee Photovoltaic Power Delivers Record Q1 FY27 Performance; PAT More Than Doubles as Margins Reach All-Time High

NSE

emmvee

BSE

544608

- Emmvee Photovoltaic Power Limited reported its strongest-ever first-quarter performance for Q1 FY27, driven by higher production volumes, deeper integration of internally manufactured TOPCon solar cells, and improved operating leverage.

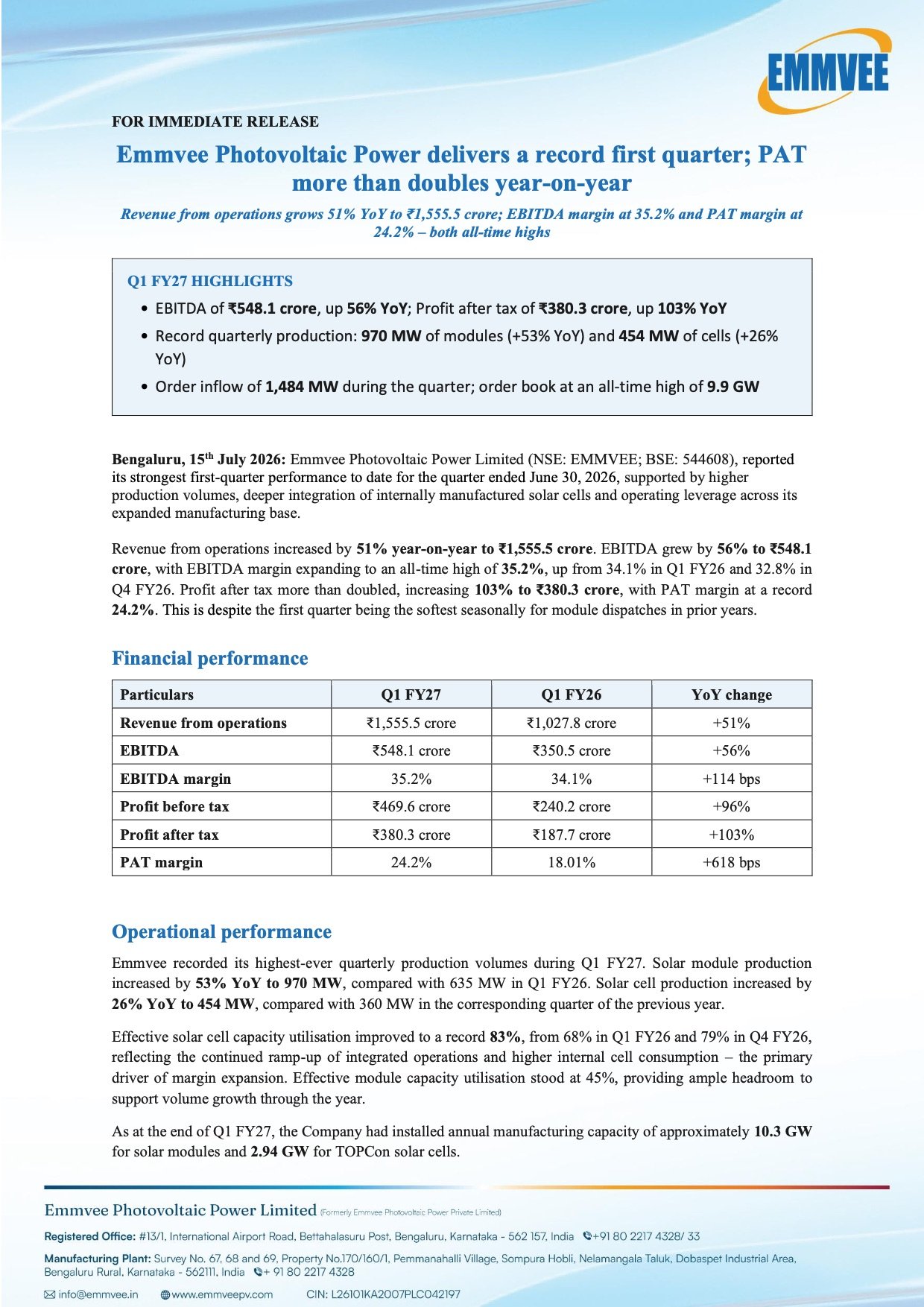

- Revenue from operations grew 51% YoY to ₹1,555.5 crore, EBITDA increased 56% YoY to ₹548.1 crore, while Profit After Tax (PAT) surged 103% YoY to ₹380.3 crore.

- The company also recorded its highest-ever quarterly module and cell production, secured 1,484 MW of fresh orders during the quarter, and ended Q1 with an all-time high order book of 9.9 GW, providing strong revenue visibility.

PRICE-SENSITIVE TRIGGER

Event: Emmvee Photovoltaic Power Limited announced its unaudited standalone and consolidated financial results for the quarter ended June 30, 2026, reporting record quarterly revenue, profitability, production volumes and order book.

Type: Quarterly Financial Results

Impact: Neutral

Immediate Effect:

- The company delivered record financial and operational performance during Q1 FY27, supported by higher manufacturing volumes, increased integration of in-house TOPCon solar cells, improved operating leverage and strong order inflows.

- The all-time high order book of 9.9 GW further strengthens revenue visibility for the coming quarters.

Financials:

Key Financial Metrics:

- Revenue from Operations: ₹1,555.5 crore (▲ 51% YoY)

- EBITDA: ₹548.1 crore (▲ 56% YoY)

- EBITDA Margin: 35.2% (vs 34.1% in Q1 FY26)

- Profit Before Tax (PBT): ₹469.6 crore (▲ 96% YoY)

- Profit After Tax (PAT): ₹380.3 crore (▲ 103% YoY)

- PAT Margin: 24.2% (vs 18.0% in Q1 FY26)

Operational Metrics:

- Solar Module Production: 970 MW (▲53% YoY)

- Solar Cell Production: 454 MW (▲26% YoY)

- Solar Cell Capacity Utilisation: 83%

- Module Capacity Utilisation: 45%

- Fresh Order Inflow: 1,484 MW

- Order Book: 9.9 GW (Record High)

- Manufacturing Capacity

- Solar Module Capacity: 10.3 GW

- TOPCon Solar Cell Capacity: 2.94 GW

Highlight:

- Emmvee delivered its strongest quarterly performance since listing, with PAT more than doubling to ₹380.3 crore, EBITDA margin expanding to a record 35.2%, and the order book reaching an all-time high of 9.9 GW.

What Happened ?

Emmvee Photovoltaic Power reported its best-ever quarterly performance, benefiting from higher production volumes, improved manufacturing efficiency and deeper integration of internally manufactured TOPCon solar cells. The increased use of captive cell production improved margins while operating leverage from expanded manufacturing facilities further enhanced profitability.

Revenue from operations grew by 51% year-on-year, while EBITDA increased 56%. Profit after tax more than doubled as the company achieved record EBITDA and PAT margins despite the first quarter historically being a seasonally weaker period for solar module dispatches.

Operationally, Emmvee recorded its highest-ever quarterly production, manufacturing 970 MW of solar modules and 454 MW of solar cells. Cell capacity utilisation improved to a record 83%, reflecting efficient utilisation of newly expanded integrated manufacturing operations.

Business momentum also remained strong, with fresh order inflows of 1,484 MW during the quarter, taking the total executable order book to an all-time high of 9.9 GW. The diversified order pipeline across independent power producers (IPPs), commercial & industrial (C&I) customers and government-linked projects provides strong revenue visibility for future quarters.

key details

Manufacturing Performance:

Emmvee achieved record production volumes during Q1 FY27, supported by improved utilisation of its integrated manufacturing facilities and continued ramp-up of TOPCon cell production.

Key Highlights:

- Solar Module Production reached 970 MW, increasing 53% YoY.

- Solar Cell Production increased to 454 MW, up 26% YoY.

- Cell manufacturing utilisation improved to 83%.

- Module manufacturing utilisation stood at 45%.

The higher utilisation of captive TOPCon cell capacity enabled better cost efficiencies while supporting higher-value module production.

Note:

- Management continues to optimize integrated manufacturing operations to improve productivity and margins.

Order Book & Business Development:

The company continued witnessing strong demand for high-efficiency solar modules.

Key Metrics:

- Fresh Order Intake during Q1 FY27: 1,484 MW

- Closing Order Book: 9.9 GW (Record High)

The robust order pipeline provides significant revenue visibility for the coming quarters and reflects continued demand across India’s expanding renewable energy sector.

Order Mix Includes:

- Utility-scale solar projects

- Independent Power Producers (IPPs)

- Commercial & Industrial (C&I) customers

- Government-backed renewable energy projects

Manufacturing Capacity:

Emmvee continued strengthening its position as one of India’s integrated solar manufacturers.

Installed Capacity:

- Solar Module Manufacturing Capacity: 10.3 GW

- TOPCon Solar Cell Manufacturing Capacity: 2.94 GW

The integrated manufacturing model allows the company to increase self-reliance, improve supply-chain efficiency and reduce dependence on imported cells.

Operational Performance:

The company’s operating performance improved significantly during the quarter.

Key Highlights:

- Higher contribution from in-house TOPCon solar cells.

- Improved manufacturing efficiencies.

- Better operating leverage from expanded capacities.

- Margin expansion despite continued investments in growth.

- Record quarterly production across both modules and cells.

Management attributed the improved profitability to operational execution rather than favourable one-off factors.

Industry Outlook:

Management highlighted continued growth opportunities driven by India’s renewable energy transition.

Growth Drivers:

- Rising domestic demand for solar power.

- Government support for local manufacturing under the “Make in India” initiative.

- Increasing adoption of high-efficiency TOPCon technology.

- Growing utility-scale and commercial solar installations.

- Continued shift towards integrated domestic manufacturing.

The company expects these structural drivers to support long-term demand for its products.

Risk Analysis

Summary:

- Although Emmvee reported record quarterly performance, the business remains influenced by execution, policy support, raw material pricing and demand dynamics within the renewable energy industry.

Key Risks:

- Delays in execution of large utility-scale solar projects.

- Volatility in prices of polysilicon, wafers and other key raw materials.

- Changes in government incentives, import duties or renewable energy policies.

- Competitive pricing pressure from domestic and international manufacturers.

- Capacity expansion and execution risks associated with rapid growth.

Worst Case:

- A slowdown in solar project execution, combined with margin pressure from rising input costs or policy changes, could reduce profitability despite a healthy order book.

Risk Level: Medium

Company Commentary

- Q1 FY27 marked the strongest first-quarter performance in the company’s history.

- Higher integration of captive TOPCon solar cells significantly supported profitability.

- Record production and order inflows reinforce confidence in future growth.

- The record 9.9 GW order book provides strong medium-term revenue visibility.

- Management remains focused on expanding manufacturing scale, improving operational efficiency and strengthening technology leadership in India’s solar manufacturing ecosystem.

Official Exchange Filing: Emmvee Photovoltaic Power Limited