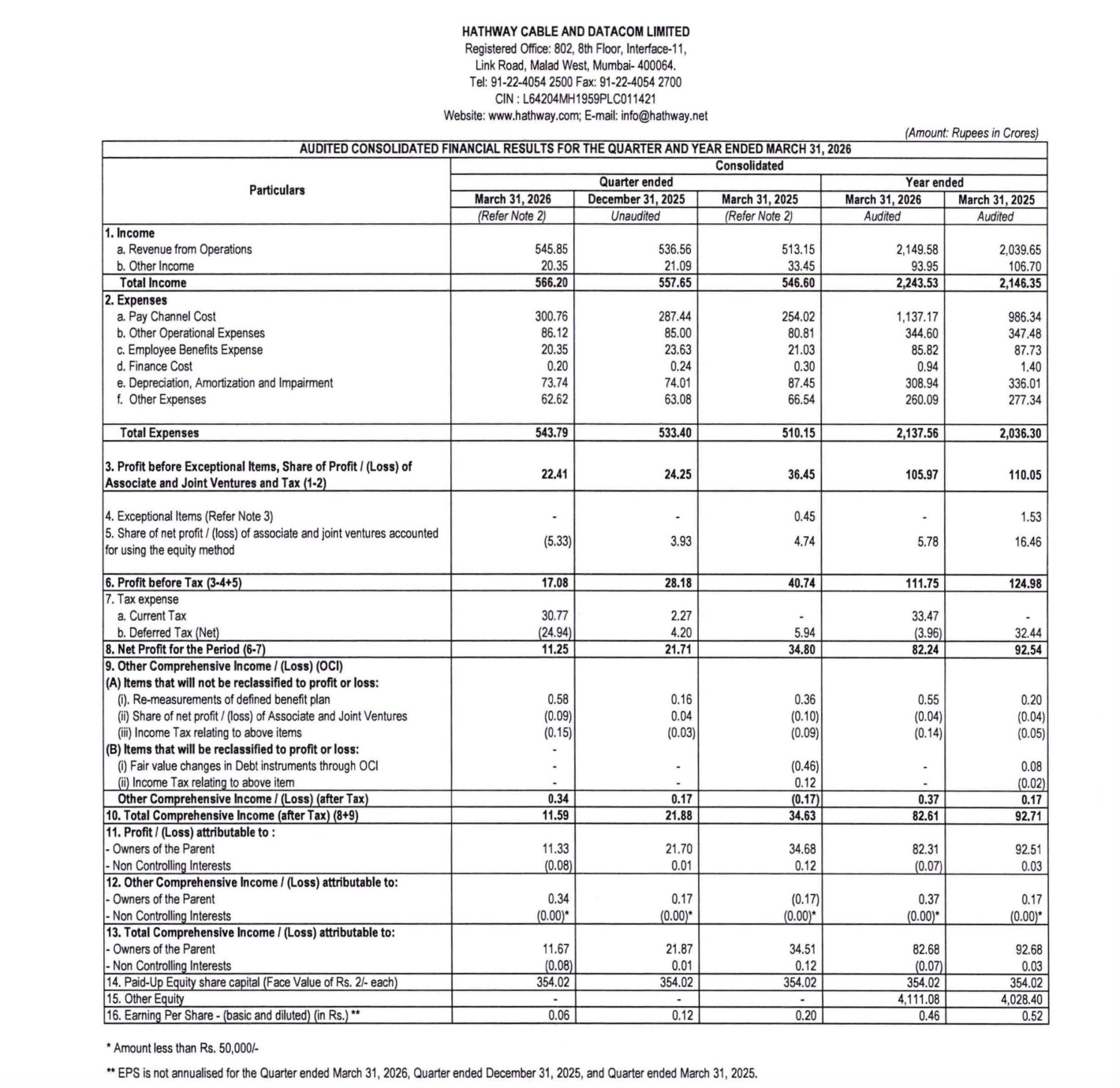

Quarter Ended: March 2026

Hathway Cable & Datacom – Q4 FY26 Results Analysis

NSE

hathway

BSE

533162

Topline improved modestly, but profit fell sharply due to margin pressure, weaker associate contribution, and elevated content/pay channel costs. Cash flows remain healthy, but earnings momentum is soft.

key financial highlights

- Revenue from Operations:

- Total Income (Q4 FY26): ₹545.85 crore

- QoQ Performance

- Previous Quarter: ₹536.56 crore

- Growth: +1.7%

- YoY Performance

- Previous Year: ₹513.15 crore

- Growth: +6.4%

- Profit After Tax (PAT):

- Current PAT: ₹11.25 crore

- QoQ

- Previous Quarter: ₹21.71 crore

- Change: -48.2%

- YoY

- Previous Year: ₹34.80 crore

- Change: -67.7%

- QoQ Trend Insight:

- Revenue Trend: Mild Growth

- Profit Trend: Sharp Decline

Margin Analysis

- Pay channel costs rose to ₹300.76 crore

- Operating expenses remain elevated

- Lower share of profit from associates

- Revenue growth insufficient to offset cost structure

Key Signal: Margin compression is significant

Segment performance

Segment Insight:

Business appears mature, with limited growth but rising cost pressure

Characteristics:

- Subscription/content cost heavy model

- Limited operating leverage visible

- Broadband/cable economics under pressure

- Associate income support weakening

Earning quality check

Positive:

- Positive operating cash flow

- Stable revenue base

- Controlled finance costs

Negative:

- Profit deterioration severe

- Weak earnings conversion

- Associate contribution falling

Interpretation: Earnings quality weakened materially, as cash generation remains better than accounting profitability

balance sheet analysis

- Total Assets: ₹5,182.36 crore

- Total Liabilities: ₹715.62 crore

Equity Growth

- FY26: ₹4,466.74 crore

- FY25: ₹4,384.08 crore

Cash Position

- FY26: ₹39.29 crore

- FY25: ₹57.27 crore

Indicates: Balance sheet remains strong due to large equity cushion, but liquidity declined

Cash flow analysis

Operating Cash Flow

- ₹198.57 crore

Investing Cash Flow

- Negative ₹209.70 crore

Financing Cash Flow

- Negative ₹6.86 crore

Closing Cash

- ₹39.29 crore

Indicates: Operating cash remains supportive, but investment outflows exceeded operating inflows

key risks

- Profit erosion risk

- Rising content/pay channel costs

- Structural pressure in cable business

- Weak operating leverage

- Declining cash reserves

management strategy

- Cost rationalization

- Broadband monetization

- Improve content economics

- Stabilize profitability

Financial Metrics

| Particular | In ₹ Crore | Q.O.Q (%) | Y.O.Y(%) |

|---|---|---|---|

| Total Income | 566.20 | +1.5 | +3.6 |

| PBT | 17.08 | -39.4 | -58.1 |

| PAT | 11.25 | -48.2 | -67.7 |

| EPS | 0.06 | -50.0 | -70.0 |

Hathway delivered modest revenue growth, but profitability deteriorated sharply

Official Exchange Filing: Hathway Cable & Datacom Limited

Quarterly Performance Context

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED