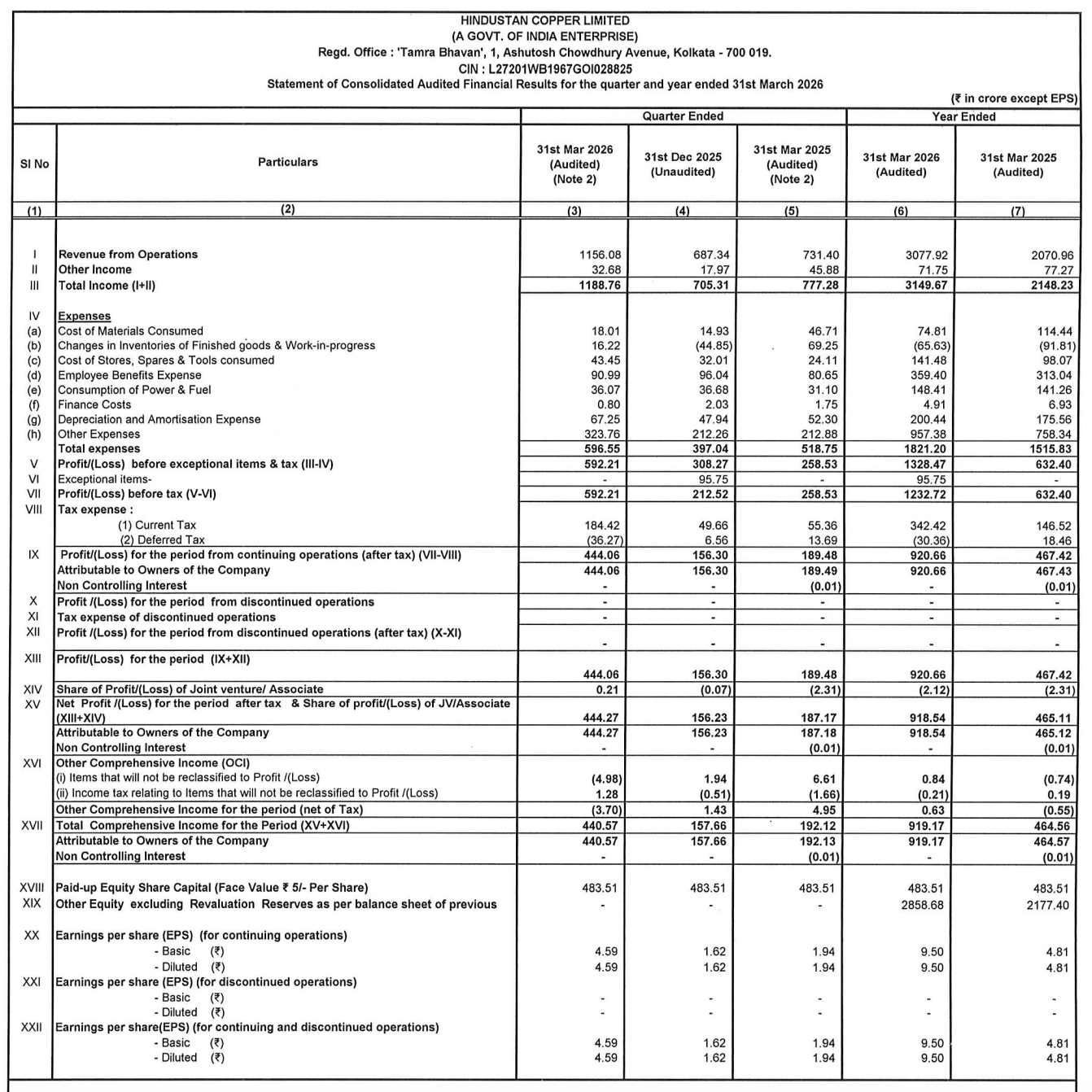

Quarter Ended: March 2026

Hindustan Copper Limited – Q4 FY26 Results

NSE

hindcopper

BSE

513599

Hindustan Copper Limited reported a sharp improvement in Q4 FY26 earnings with strong revenue growth, expanding profitability, and significantly improved operational cash generation.

key financial highlights

- Revenue from Operations:

- Revenue (Q4 FY26): ₹1,156.08 Crores

- QoQ Change: +68.20%

- YoY Change: +58.06%

- Previous Quarter (Q3 FY26): ₹687.34 Crores

- Previous Year (Q4 FY25): ₹731.40 Crores

- Revenue (Q4 FY26): ₹1,156.08 Crores

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹444.27 Crores

- QoQ Change: +184.26%

- YoY Change:+137.35%

- Previous Quarter (Q3 FY26): ₹156.23 Crores

- Previous Year (Q4 FY25): ₹187.17 Crores

- PAT (Q4 FY26): ₹444.27 Crores

- QoQ Performance:

- Revenue Trend: Sequential revenue growth remained exceptionally strong due to operational ramp-up and stronger business momentum.

- Profit Trend: Profit expanded significantly on account of better operating margins and higher contribution from core mining activities.

- Revenue Trend: Sequential revenue growth remained exceptionally strong due to operational ramp-up and stronger business momentum.

Margin Analysis

Drivers:

- Significant revenue growth improved operating leverage.

- Employee and operating costs remained proportionately controlled.

- Lower finance costs supported earnings growth.

- Better inventory management improved operational efficiency.

- Strong operating cash generation strengthened profitability quality.

Insight:

- The company witnessed meaningful margin expansion driven by higher operational utilization and stronger revenue conversion into profits.

Segment insight

Business Summary:

The company continues to focus on copper mining expansion, ore production enhancement, and strengthening domestic copper supply capabilities.

Key Characteristics:

- Government-owned copper producer.

- Mining-led operational business model.

- Commodity-linked revenue exposure.

- Expansion-oriented capex strategy.

- Strong linkage with infrastructure and industrial demand.

Earning quality check

Key Drivers:

- Operating cash flow increased substantially YoY.

- Net cash from operations rose to ₹1,473.56 crore.

- Cash and cash equivalents increased significantly.

- Lower debt obligations improved financial flexibility.

- Profit growth aligned with operational cash generation.

Interpretations:

- Earnings quality remained healthy with strong operational cash conversion and substantial liquidity improvement indicating sustainable operational performance.

balance sheet Analysis

- Total Assets: ₹4,415.68 Crores

- Total Liabilities: ₹1,073.48 Crores

Insight:

- The company strengthened its balance sheet through higher retained earnings, improved cash reserves, and controlled liabilities, reflecting stronger financial stability.

key risks

- Copper price volatility in global commodity markets.

- Regulatory and environmental clearance risks.

- Mining expansion execution risks.

- Operational disruptions in mining activities.

- Dependence on industrial demand cycles.

- Commodity-linked margin fluctuations.

management strategy signals

Focus Area:

- Expanding mining production capacity.

- Increasing ore extraction efficiency.

- Strengthening domestic copper production.

- Enhancing operational productivity.

- Maintaining financial discipline.

- Supporting long-term mining expansion projects.

Financial metrics table

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹1,188.76 Crores | +68.55% | +52.94% |

| PBT | ₹592.21 Crores | +179.11% | +128.93% |

| PAT | ₹444.27 Crores | +184.26% | +137.35% |

Hindustan Copper Limited delivered an exceptionally strong Q4 FY26 performance with sharp growth in revenue, profitability, and operating cash flow. The company’s improving balance sheet, rising cash reserves, and operational expansion strategy position it favorably for future growth amid rising domestic copper demand.

Official Exchange Filing: Hindustan Copper Limited

Quarterly Performance Context

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED