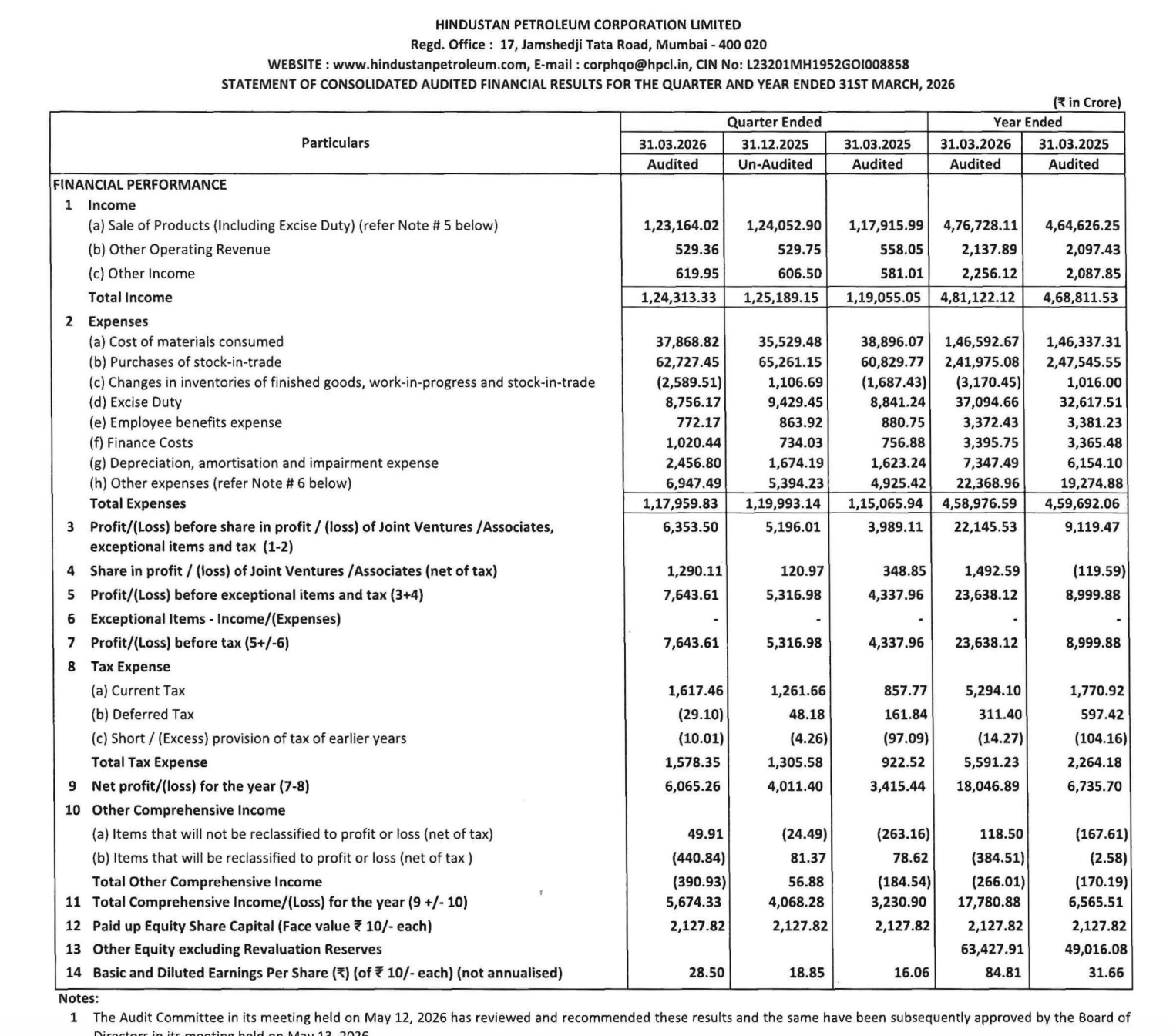

Quarter Ended: March 2026

Hindustan Petroleum Corporation Limited – Q4 FY26 Results

NSE

hpcl

BSE

500104

HPCL reported strong YoY and QoQ profitability growth in Q4 FY26 supported by improved downstream petroleum performance, higher associate contribution, and operational efficiencies despite volatile crude-linked cost structures.

key financial highlights

- Revenue from Operations:

- Revenue (Q4 FY26): ₹1,23,693.38 Cr

- QoQ Change: -0.71%

- YoY Change: +4.40%

- Previous Quarter (Q3 FY26): ₹1,24,582.65 Cr

- Previous Year (Q4 FY25): ₹1,18,474.04 Cr

- Revenue (Q4 FY26): ₹1,23,693.38 Cr

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹6,065.26 Cr

- QoQ Change: +51.20%

- YoY Change: +77.58%

- Previous Quarter (Q3 FY26): ₹4,011.40 Cr

- Previous Year (Q4 FY25): ₹3,415.44 Cr

- PAT (Q4 FY26): ₹6,065.26 Cr

- QoQ Performance:

- Revenue: Stable to Slightly Negative

- Profit: Strongly Positive

Margin Analysis

Drivers:

- Lower inventory losses versus prior comparable periods

- Strong contribution from downstream petroleum segment

- Improved share of profit from joint ventures and associates

- Controlled finance cost growth despite large operational scale

- Better operational leverage due to refining and marketing efficiencies

Insight:

- Profit growth significantly outpaced revenue growth, indicating strong margin expansion and operational efficiency improvement.

Segment performance

Segments: Downstream Petroleum

- Revenue: ₹1,23,594.73 Cr

- Insights:

- Core business continued dominating overall revenue mix

- Segment profitability improved sharply YoY

- Refining and fuel marketing operations remained the primary earnings driver

Segments: Other Segment

- Revenue: ₹159.36 Cr

- Insights:

- Non-core operations remained relatively insignificant

- Segment continued to report losses but impact remained limited

Segment insight

Business Summary:

HPCL remains heavily dependent on downstream petroleum operations with minimal diversification contribution. Earnings strength was primarily generated through refining and fuel marketing activities.

Key Characteristics:

- Single dominant operating segment

- High sensitivity to crude oil and refining margins

- PSU-led operational stability

- Large-scale integrated petroleum operations

Earning quality check

Key Drivers:

- Operating cash flow rose strongly to ₹36,110.68 Cr for FY26

- Profit before tax increased to ₹23,638.12 Cr for FY26

- Associate and JV contribution improved materially

- Non-cash adjustments remained manageable

- Finance cost growth stayed controlled relative to earnings expansion

Interpretations:

- The earnings quality appears healthy as profitability growth was backed by stronger operating cash generation and improved operational metrics rather than only accounting adjustments.

balance sheet Analysis

- Total Assets: ₹2,03,039.24 Cr

- Total Liabilities: ₹1,37,483.12 Cr

Insight:

- Total assets increased from ₹1,94,744.64 Cr to ₹2,03,039.24 Cr

- Equity strengthened sharply to ₹65,556.12 Cr

- Current borrowings reduced significantly from ₹31,778.11 Cr to ₹15,428.33 Cr

- Net worth expansion reflects strong retained earnings generation

- Working capital structure improved versus previous year

Cash flow analysis

Operating Cash Flow:

- Net Cash from Operating Activities : ₹36,110.68 Cr

- Strong operational cash generation reflects healthier profitability and better working capital management.

Investing Cash Flow:

- Net Cash Used in Investing Activities : ₹11,403.94 Cr

- Key Observations:

- Continued investment in property, plant, and equipment

- Strategic investments in associates and ventures continued

- Capex intensity remained elevated

Financing Cash Flow:

- Net Cash Used in Financing Activities : ₹22,770.27 Cr

- Key Observations:

- Significant repayment of long-term and short-term borrowings

- Dividend payout remained substantial

- Balance sheet deleveraging trend visible

key risks

- High dependence on crude oil price movements

- Refining margin volatility risk

- Government policy and fuel pricing intervention risk

- Inventory gain/loss fluctuations impacting quarterly profitability

- Large capital expenditure and infrastructure funding requirements

management strategy signals

Focus Area:

- Strengthening downstream petroleum operations

- Improving operational efficiencies

- Managing borrowing profile and leverage

- Expanding strategic investments and joint ventures

- Enhancing cash flow generation

Financial metrics table

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹1,24,313.33 Cr | -0.70% | +4.42% |

| PBT | ₹7,643.61 Cr | +43.76% | +76.20% |

| PAT | ₹6,065.26 Cr | +51.20% | +77.58% |

HPCL delivered a strong Q4 FY26 performance with substantial profit growth, stronger cash generation, improving balance sheet quality, and better operational efficiency.

While revenue growth remained moderate, margin expansion and lower leverage strengthened overall financial positioning. The company remains exposed to commodity cycle volatility, but operational execution during the quarter was robust.

Official Exchange Filing: Hindustan Petroleum Corporation Limited

Quarterly Performance Context

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED