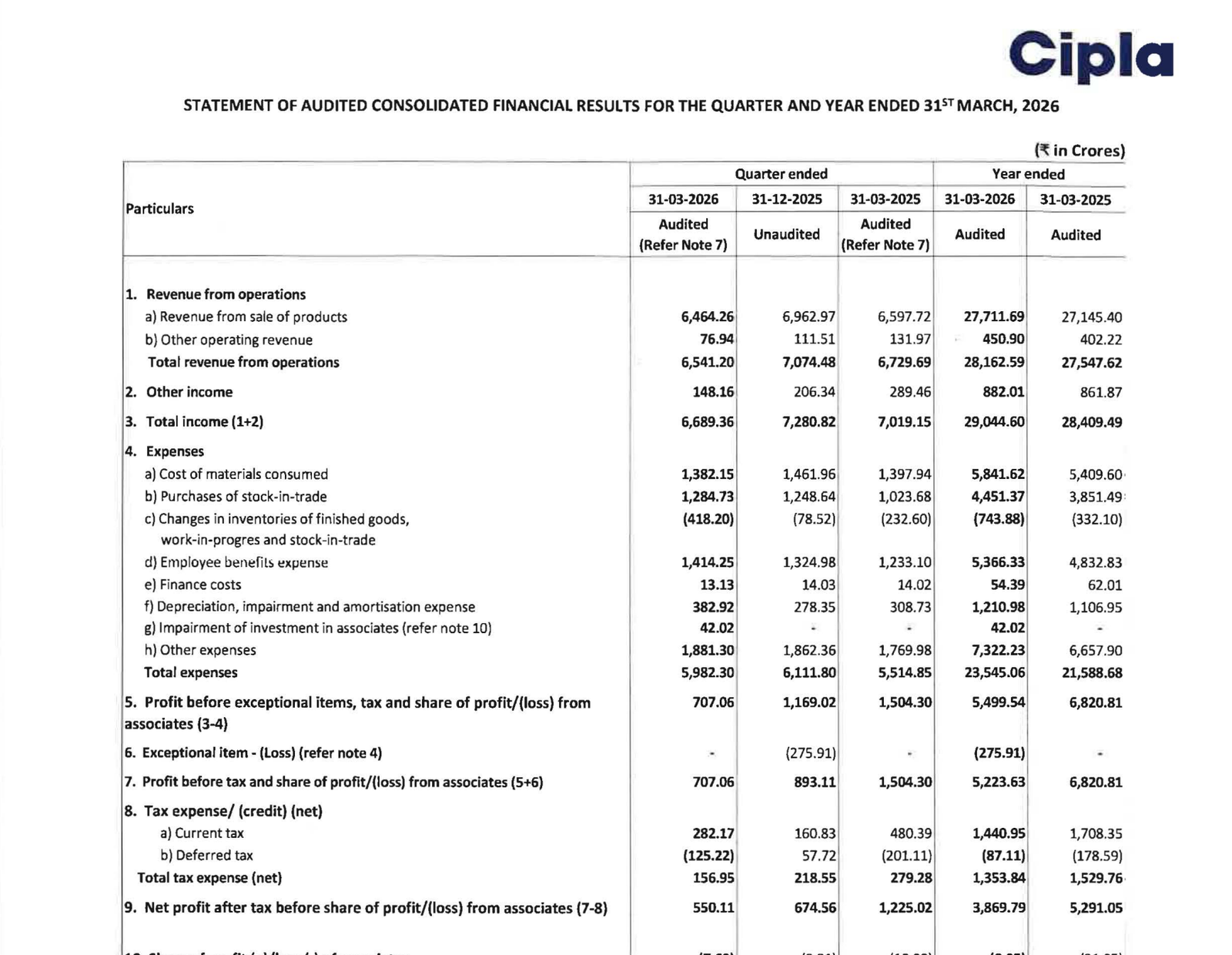

Quarter Ended: March 2026

Cipla Limited – Q4 FY26 Results

NSE

cipla

BSE

500087

Cipla reported a weaker Q4 FY26 performance with revenue declining sequentially and profitability falling sharply YoY due to higher operating expenses, impairment charges, and margin compression despite healthy annual revenue expansion.

key financial highlights

- Revenue from Operations:

- Revenue (Q4 FY26): ₹6,541.20 Cr

- QoQ Change: -7.54%

- YoY Change: -2.80%

- Previous Quarter (Q3 FY26): ₹7,074.48 Cr

- Previous Year (Q4 FY25): ₹6,729.69 Cr

- Revenue (Q4 FY26): ₹6,541.20 Cr

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹542.51 Cr

- QoQ Change: -19.54%

- YoY Change: -55.32%

- Previous Quarter (Q3 FY26): ₹674.25 Cr

- Previous Year (Q4 FY25): ₹1,214.14 Cr

- PAT (Q4 FY26): ₹542.51 Cr

- QoQ Performance:

- Revenue: Negative

- Profit: Strongly Positive

Margin Analysis

Drivers:

- Employee benefit expenses increased materially

- Other operating expenses remained elevated

- Impairment charge relating to investment in associates impacted earnings

- Revenue decline reduced operating leverage benefits

- Higher depreciation and amortisation expenses affected margins

Insight:

- Margins compressed significantly as expense growth outpaced revenue generation during the quarter.

Segment insight

Business Summary:

Cipla continues operating as a diversified pharmaceutical company with strong exposure across domestic formulations, respiratory therapies, branded generics, and international markets.

Key Characteristics:

- Strong domestic pharmaceutical franchise

- Global generics exposure

- High regulatory dependency

- R&D-driven business model

- Margin-sensitive to product mix and compliance costs

Earning quality check

Key Drivers:

- Operating cash flow remained healthy at ₹3,940.02 Cr

- PAT weakened materially despite stable annual revenue growth

- Working capital adjustments impacted operational efficiency

- Higher impairment and operating costs affected earnings conversion

- Cash reserves and investments strengthened balance sheet quality

Interpretations:

- Earnings quality remains moderate. While cash generation stayed stable, profitability compression and impairment charges weakened overall earnings strength.

balance sheet Analysis

- Total Assets: ₹42,495.98 Cr

- Total Liabilities: ₹7,975.74 Cr

Insight:

- Equity increased strongly to ₹34,520.24 Cr

- Cash and cash equivalents rose to ₹1,018.22 Cr

- Investments increased to ₹7,679.42 Cr

- Borrowings remained extremely low relative to balance sheet size

- Overall leverage profile stayed highly conservative

Cash flow analysis

Operating Cash Flow:

- Net Cash Generated from Operating Activities : ₹3,940.02 Cr

- Operating cash flow remained strong though lower than FY25 due to profitability moderation and working capital changes.

Investing Cash Flow:

- Net Cash Used in Investing Activities : ₹2,326.13 Cr

- Key Observations:

- Continued investment in property, plant, and equipment

- Higher investment into intangible assets and acquisitions

- Increase in treasury and investment deployment activities

Financing Cash Flow:

- Net Cash Used in Financing Activities : ₹1,233.65 Cr

- Key Observations:

- Dividend payout remained significant

- Borrowing levels stayed low

- Financing structure continued conservative

key risks

- Pricing pressure in global generic markets

- Regulatory and compliance risks

- Currency fluctuation exposure

- Margin pressure from rising operational costs

- Product concentration and competitive intensity

management strategy signals

Focus Area:

- Expanding global pharmaceutical presence

- Strengthening respiratory and specialty portfolio

- Enhancing R&D capabilities

- Maintaining strong cash generation

- Strategic investment allocation and operational efficiency

Financial metrics table

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹6,689.36 Cr | -8.12% | -4.70% |

| PBT | ₹707.06 Cr | -20.83% | -55.99% |

| PAT | ₹542.51 Cr | -19.54% | -55.32% |

Cipla’s Q4 FY26 performance reflected short-term profitability pressure despite maintaining a fundamentally strong balance sheet and healthy operating cash flows. Revenue softness, impairment charges, and elevated operational expenses impacted margins sharply.

However, the company continues to maintain financial stability, low leverage, and strategic investment capacity, supporting long-term pharmaceutical sector positioning.

Official Exchange Filing: Cipla Limited

Quarterly Performance Context

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED