Financial Results

JSW Cement Reports Strong FY26 Growth with 44% Surge in Operating EBITDA and Expansion Momentum

NSE

jswcement

BSE

544480

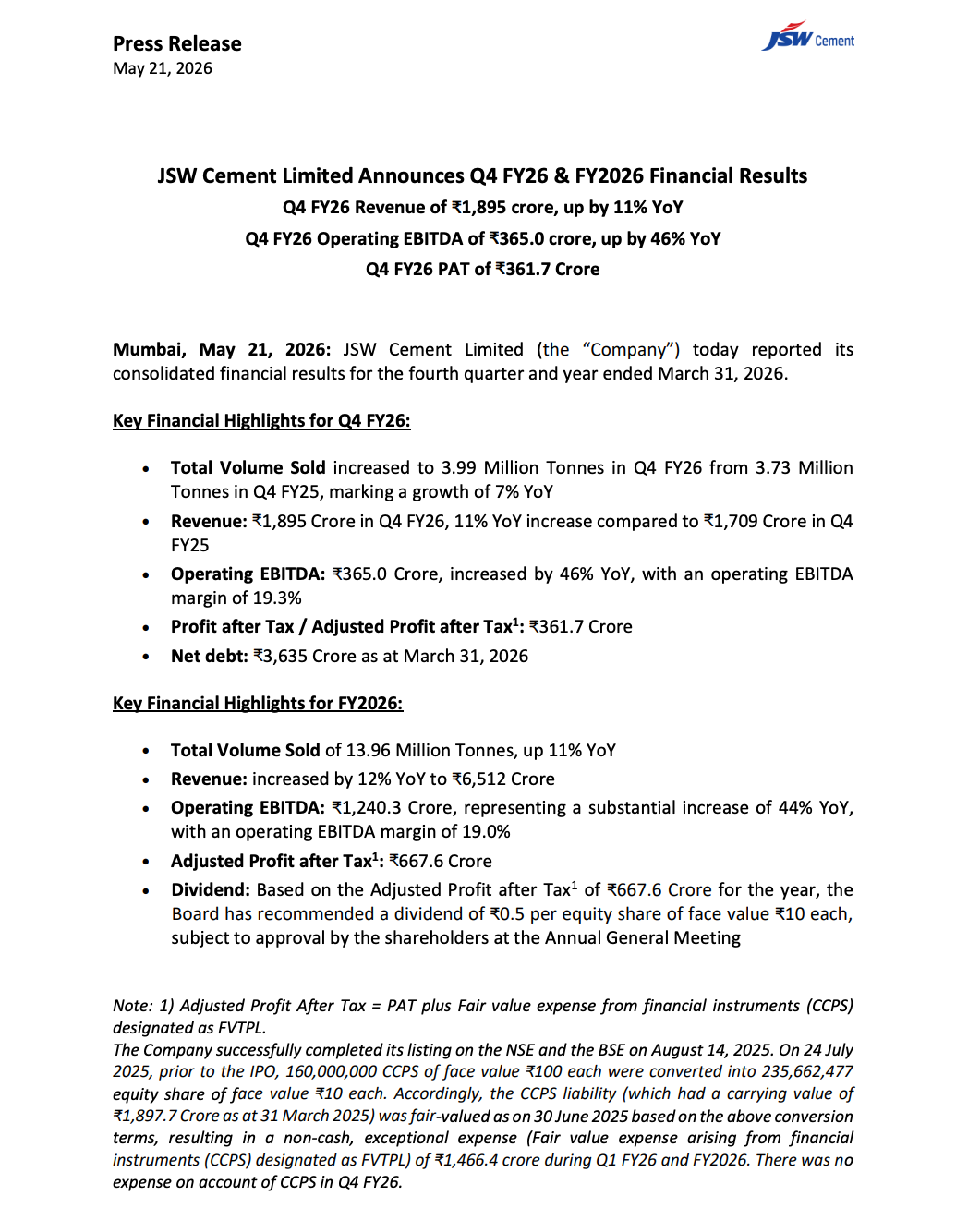

JSW Cement Limited announced its audited Q4 FY26 and FY26 financial results, reporting strong operational and profitability growth. FY26 revenue increased 12% YoY to ₹6,512 crore, while operating EBITDA surged 44% YoY to ₹1,240.3 crore. The company also continued aggressive expansion through new clinker and grinding capacities.

PRICE-SENSITIVE TRIGGER

Event: Q4 FY26 and FY26 Audited Financial Results Announcement

Type: Financial Results

Impact: Positive

Immediate Effect: The company delivered strong operational growth, improved margins, increased cement volumes, and accelerated capacity expansion, strengthening its long-term market position in the Indian cement sector.

Key Metrics:

- Q4 FY26 Revenue: ₹1,895 Crore

- Q4 FY25 Revenue: ₹1,709 Crore

- Q4 Revenue Growth YoY: 11%

- Q4 FY26 Operating EBITDA: ₹365.0 Crore

- Q4 EBITDA Growth YoY: 46%

- Q4 EBITDA Margin: 19.3%

- Q4 Operating EBITDA per Ton: ₹916 per ton

- Q4 Adjusted EBITDA: ₹378.4 Crore

- Q4 Total EBITDA (Including Other Income): ₹385.6 Crore

- Q4 FY26 PAT / Adjusted PAT: ₹361.7 Crore

- FY26 Revenue: ₹6,512 Crore

- FY26 Revenue Growth YoY: 12%

- FY26 Operating EBITDA: ₹1,240.3 Crore

- FY26 EBITDA Growth YoY: 44%

- FY26 EBITDA Margin: 19.0%

- FY26 EBITDA per Ton: ₹888 per ton

- FY26 Total EBITDA (Including Other Income): ₹1,392.7 Crore

- FY26 Adjusted PAT: ₹667.6 Crore

- Q4 FY26 Total Volume Sold: 3.99 Million Tonnes

- Q4 FY26 Cement Volume Sold: 2.35 Million Tonnes

- Q4 Cement Volume Growth YoY: 12%

- Q4 GGBS Volume Sold: 1.57 Million Tonnes

- FY26 Total Volume Sold: 13.96 Million Tonnes

- FY26 Cement Volume Sold: 7.73 Million Tonnes

- FY26 GGBS Volume Sold: 5.78 Million Tonnes

- Net Debt (March 31, 2026): ₹3,635 Crore

- Dividend Recommended: ₹0.5 per equity share

- FY26 Capex: ₹1,962 Crore

- Q4 FY26 Capex: ₹506 Crore

- Current Grinding Capacity: 24.10 MTPA

- Current Clinker Capacity: 9.74 MTPA

- Target Grinding Capacity: 46.00 MTPA

- Target Clinker Capacity: 13.04 MTPA

Highlight Metric:

- FY26 operating EBITDA surged 44% YoY to ₹1,240.3 crore while EBITDA margin improved to 19.0%.

What Happened ?

JSW Cement Limited announced strong Q4 FY26 and FY26 financial results driven by higher cement volumes, improved operational efficiencies, and expansion-led growth.

For Q4 FY26:

- Revenue increased 11% YoY to ₹1,895 crore.

- Operating EBITDA rose 46% YoY to ₹365 crore.

- EBITDA margin improved significantly to 19.3%.

- Cement sales volume grew 12% YoY to 2.35 million tonnes.

- Total volume sold increased 7% YoY to 3.99 million tonnes.

- PAT / Adjusted PAT stood at ₹361.7 crore.

For FY26:

- Revenue increased 12% YoY to ₹6,512 crore.

- Operating EBITDA surged 44% YoY to ₹1,240.3 crore.

- Adjusted PAT reached ₹667.6 crore.

- Total sales volume rose 11% YoY to 13.96 million tonnes.

- Cement sales volume increased 9% YoY to 7.73 million tonnes.

- GGBS sales volume grew 12% YoY to 5.78 million tonnes.

The company also announced progress on expansion projects, including commissioning of the first phase of the Nagaur integrated cement unit in Rajasthan and approval for additional grinding capacity expansion.

JSW Cement further confirmed adoption of the new tax regime beginning FY27, leading to deferred tax liability reduction recognition of ₹211.21 crore during FY26.

Key Details

Operational Growth, Capacity Expansion & Strategic Developments:

- FY26 business updates included:

- Launch of super-premium cement products in Southern and Eastern India.

- Successful IPO completion on NSE and BSE in August 2025.

- Commissioning of Shiva Cement’s 1 MTPA grinding unit at Sambalpur, Odisha.

- Commencement of production at Nagaur integrated cement plant in Rajasthan.

- Preferred bidder status for Sikilangso limestone mining leases in Assam.

- Nagaur plant details:

- 3.3 MTPA clinkerisation capacity.

- Initial 2.5 MTPA grinding capacity.

- Additional approved expansion:

- 2.5 MTPA cement grinding capacity at Nagaur.

- Post expansion Nagaur grinding capacity:

- 6.0 MTPA.

- Estimated investment for expansion:

- ₹430 crore.

- Company expansion target:

- 46.00 MTPA grinding capacity.

- 13.04 MTPA clinker capacity.

- Sustainability achievements:

- Lowest CO2 emission intensity among peers at 268 kg CO2 per ton.

- Awards & recognitions:

- Shiva Cement received British Safety Council distinction award.

- Vijayanagar unit received “Legend (Emerging)” safety award.

- Golden Peacock Award for Innovation Management.

- Global operations:

- Nine plants across India.

- Operations in UAE through JSW Cement FZC.

- Product portfolio includes:

- PSC.

- PCC.

- PPC.

- OPC.

- GGBS.

- Clinker.

- Construction chemicals.

- Ready mix concrete.

Note:

- The company highlighted that strong operational leverage, disciplined capacity expansion, and sustainable manufacturing practices are driving long-term growth and profitability improvements.

Risk Analysis

Summary:

- Despite strong earnings growth, the company remains exposed to industry cyclicality, raw material inflation, infrastructure demand fluctuations, and expansion execution risks.

Key Risks:

- Cement demand remains sensitive to infrastructure and real estate cycles.

- Large expansion projects involve execution and capital allocation risks.

- Rising fuel and freight costs may pressure margins.

- High capex commitments could impact leverage if demand slows.

- Competitive intensity in the cement industry remains elevated.

- Regulatory and environmental compliance costs may increase.

- Volatility in foreign exchange rates may impact borrowing costs and profitability.

Worst Case Scenario:

- If infrastructure demand weakens or capacity expansion utilization slows, the company may face pressure on margins, debt levels, and return ratios despite higher installed capacities.

Risk Level: Medium

Company Commentary

- Management stated that FY26 delivered strong volume growth and profitability improvement.

- The company highlighted continued progress on pan-India expansion strategy.

- JSW Cement emphasized operational efficiency improvements and margin expansion.

- Management confirmed ongoing investments toward sustainable and low-carbon cement manufacturing.

- The company reiterated focus on scaling clinker and grinding capacities aggressively.

- Management highlighted confidence in long-term demand outlook for the Indian cement industry.

Official Exchange Filing: JSW Cement Limited