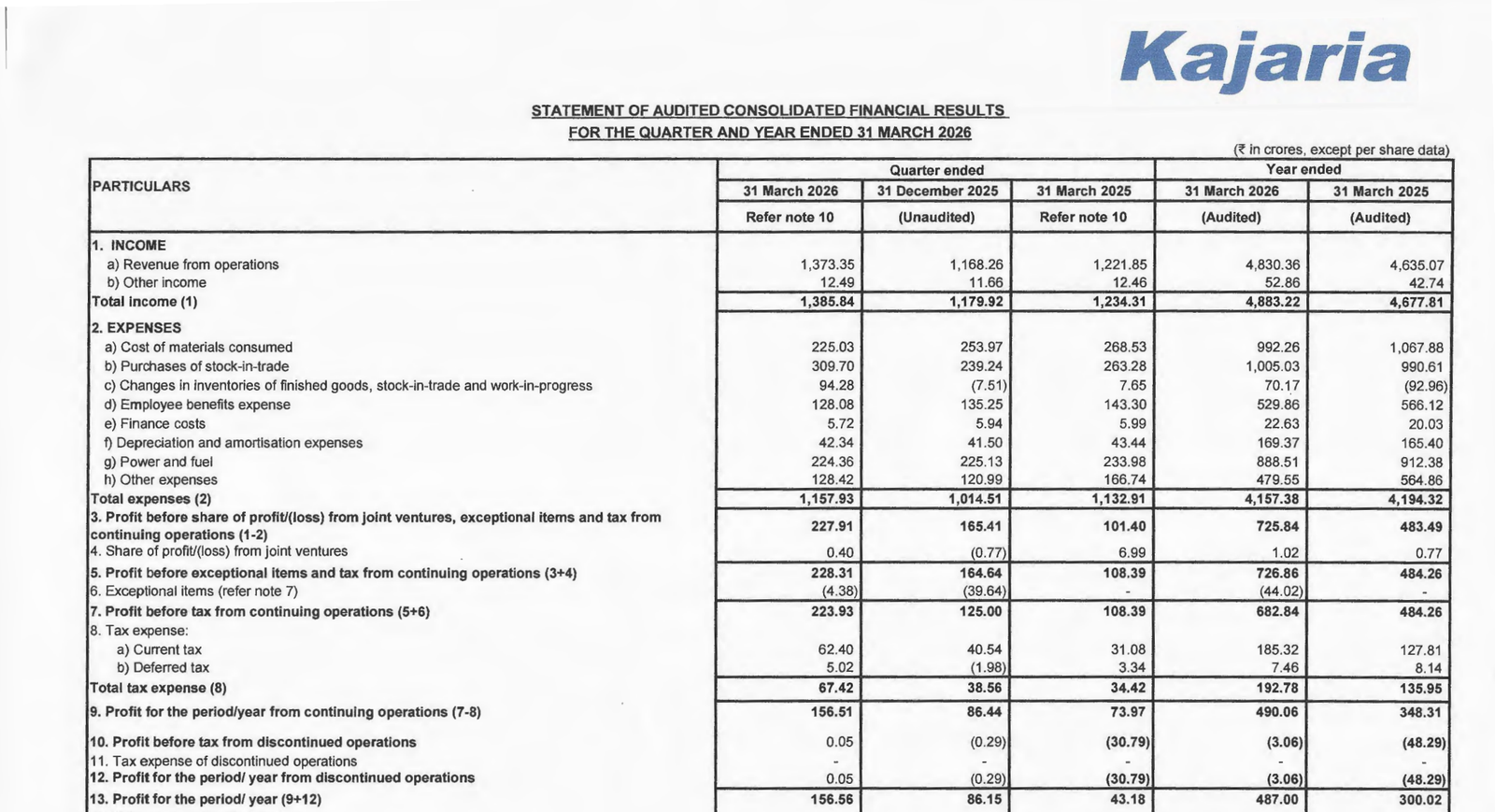

Quarter Ended: March 2026

Kajaria Ceramics Q4 FY26 Results

NSE

kajariacer

BSE

500233

Kajaria delivered consistent revenue growth with sharp improvement in profitability, supported by strong Tiles segment execution and operating leverage.

key financial highlights

- Revenue from Operations:

- Revenue (Q4 FY26): ₹1,373.35 Cr

- QoQ Change: +17.6%

- YoY Change: +12.4%

- Previous Quarter (Q3 FY26): ₹1,168.26 Cr

- Previous Year (Q4 FY25): ₹1,221.85 Cr

- Revenue (Q4 FY26): ₹1,373.35 Cr

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹156.56 Cr

- QoQ Change: +81.6%

- YoY Change: +262.6%

- Previous Quarter (Q3 FY26): ₹86.15 Cr

- Previous Year (Q4 FY25): ₹43.18 Cr

- PAT (Q4 FY26): ₹156.56 Cr

- QoQ Performance

- Revenue Trend: Strong growth

- Profit Trend: Sharp improvement

Margin Analysis

Drivers:

- Better operating leverage due to higher volumes

- Stabilization in fuel and raw material costs

- Controlled employee and overhead expenses

Insight:

- Margins are expanding significantly, indicating efficiency improvement and pricing discipline

Segment performance

Segment: Tiles

- Revenue: ₹1,212.67 Cr

- Insights:

- Core growth driver (~88% contribution)

- Strong QoQ and YoY expansion

- Improved segment profitability

Segment: Other (Adhesives, sanitary-ware etc. )

- Revenue: ₹1,212.67 Cr

- Insights:

- Core growth driver (~88% contribution)

- Strong QoQ and YoY expansion

- Improved segment profitability

Segment insight

Summary:

- Tiles segment dominates Kajaria’s business with consistent demand and margin expansion, while other segments provide incremental growth

Charcateristics:

- Tiles = high volume, stable margin business

- Others = growth optionality

- Brand-led pricing power

- Distribution-driven scale

Earning quality check

Drivers:

- Profit driven by core operations (Tiles)

- Minimal dependence on non-operating income

- No major exceptional distortions

Interpretations:

- High-quality earnings with strong operational backing and improving margin profile

balance sheet Analysis

- Total Assets: ₹4,029.21 Cr

- Total Liabilities: ₹898.73 Cr

Insight:

- Strong balance sheet with low leverage and healthy equity base, indicating financial stability

key risks

- Raw material & gas price volatility

- Real estate demand slowdown

- Competitive pricing pressure

- Dependence on Tiles segment

management strategy signals

Focus Area:

- Strengthening Tiles dominance

- Expanding adhesives & sanitaryware

- Cost optimization

- Distribution expansion

Financial metrics table

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Revenue | ₹1,373 Cr | +17.6% | +12.4% |

| Total Expense | ₹1,157.93 Cr | +14.1% | +2.2% |

| Net Profit | ₹156.56 Cr | +81.6% | +262.6% |

Kajaria Ceramics has delivered a strong quarter with healthy revenue growth and sharp margin expansion. The Tiles segment continues to dominate performance, while improving profitability indicates better cost control and operating leverage. The company remains fundamentally strong with a positive outlook

Official Exchange Filing: Kajaria Ceremics Ltd

Quarterly Performance Context

COST OF OPERATIONS AS % OF REVENUE

84%

NET PROFIT AS % OF REVENUE

11%

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED