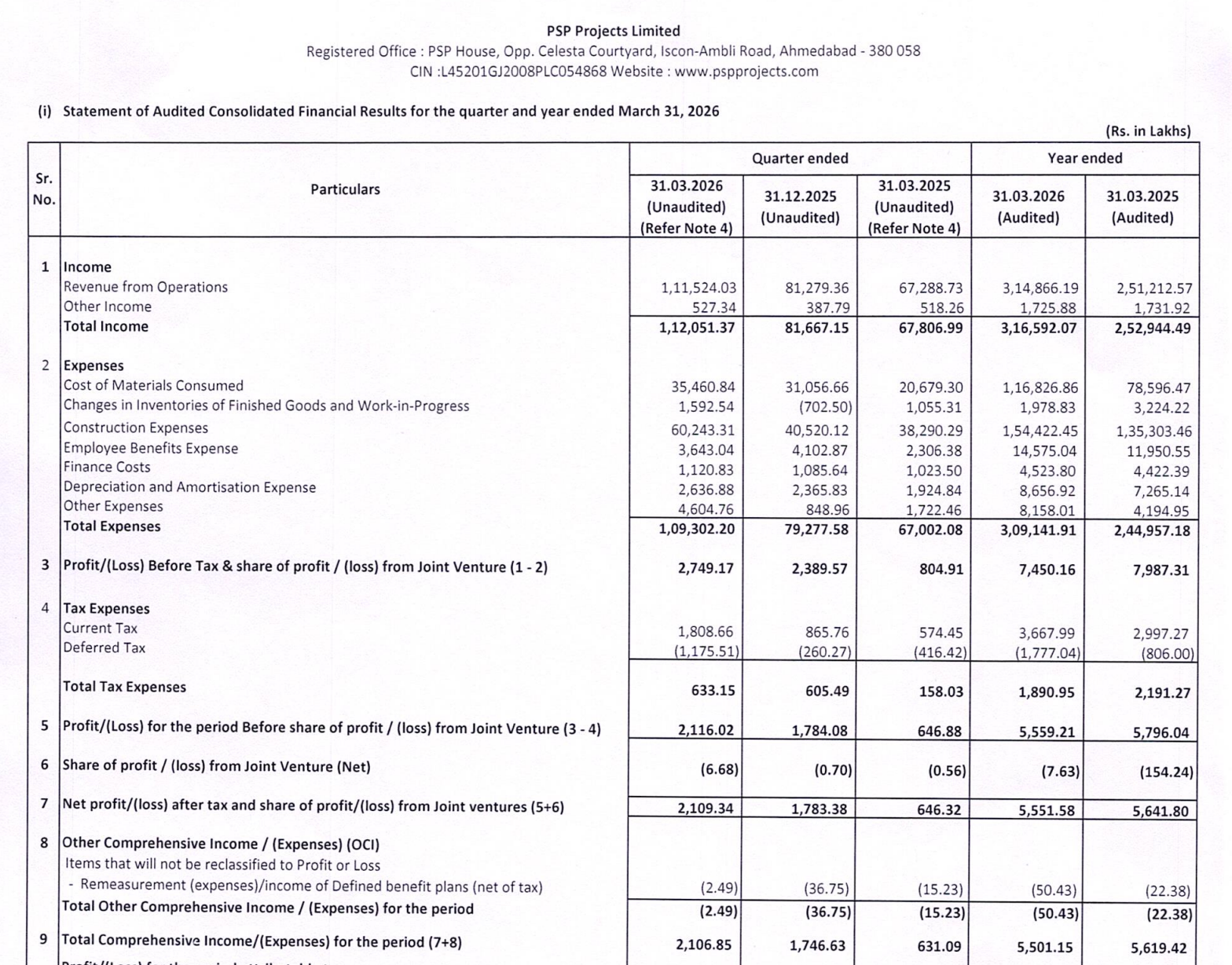

Quarter Ended: March 2026

PSP Projects – Q4 FY26 Results

NSE

pspproject

BSE

540544

Execution momentum is strong with robust revenue growth, but margin pressures and working capital intensity remain key concerns

key financial highlights

- Revenue from Operations:

- Revenue (Q4 FY26): ₹1,11,524.03 Lakh

- QoQ Change: +37.2%

- YoY Change: +65.7%

- Previous Quarter (Q3 FY26): ₹81,279.36 Lakh

- Previous Year (Q4 FY25): ₹67,288.73 Lakh

- Revenue (Q4 FY26): ₹1,11,524.03 Lakh

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹2,109.34 Lakh

- QoQ Change: +18.3%

- YoY Change: +226.0%

- Previous Quarter (Q3 FY26): ₹1,783.38 Lakh

- Previous Year (Q4 FY25): ₹646.32 Lakh

- PAT (Q4 FY26): ₹2,109.34 Lakh

- QoQ Performance

- Revenue Trend: Strong growth

- Profit Trend: Improving

Margin Analysis

Drivers:

- Higher construction expenses scaling with execution

- Increase in employee & material costs

- Operating leverage partially supporting margins

Insight:

- Margins are recovering QoQ but remain structurally tight due to EPC nature

Segment insight

Summary:

- PSP Projects operates in EPC (Engineering, Procurement, Construction), driven by project execution cycles

Charcateristics:

- High working capital business

- Revenue linked to project milestones

- Margin-sensitive to input costs

- Order book-driven visibility

Earning quality check

Drivers:

- Earnings driven by core construction activity

- No major exceptional items

- Improvement supported by execution scale

Interpretations:

- Earnings quality is operationally driven but dependent on execution efficiency and cost control

balance sheet Analysis

- Total Assets: ₹3,08,887.82 Lakhs

- Total Liabilities: ₹1,82,492.63 Lakhs

Insight:

- Balance sheet expanded significantly due to working capital build-up (receivables & cash increase)

key risks

- High working capital intensity (receivables spike)

- Execution delays impacting cash flows

- Cost inflation in raw materials

- Dependency on order inflows

management strategy signals

Focus Area:

- Scaling project execution

- Improving working capital cycle

- Maintaining order book growth

Financial metrics table

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Revenue | ₹1,115 Cr | +37.2% | +65.7% |

| Total Expense | ₹1,093 Cr | +37.1% | +63.0% |

| Net Profit | ₹21.1 Cr | +18.3% | +226.0% |

PSP Projects is showing strong execution-led growth with sharp revenue expansion and improving profitability. However, margins remain thin and working capital intensity is rising sharply, which could impact cash flows. The story remains execution-driven with moderate risk-reward.

Official Exchange Filing: PSP Project Ltd

Quarterly Performance Context

COST OF OPERATIONS AS % OF REVENUE

98%

NET PROFIT AS % OF REVENUE

2%

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED