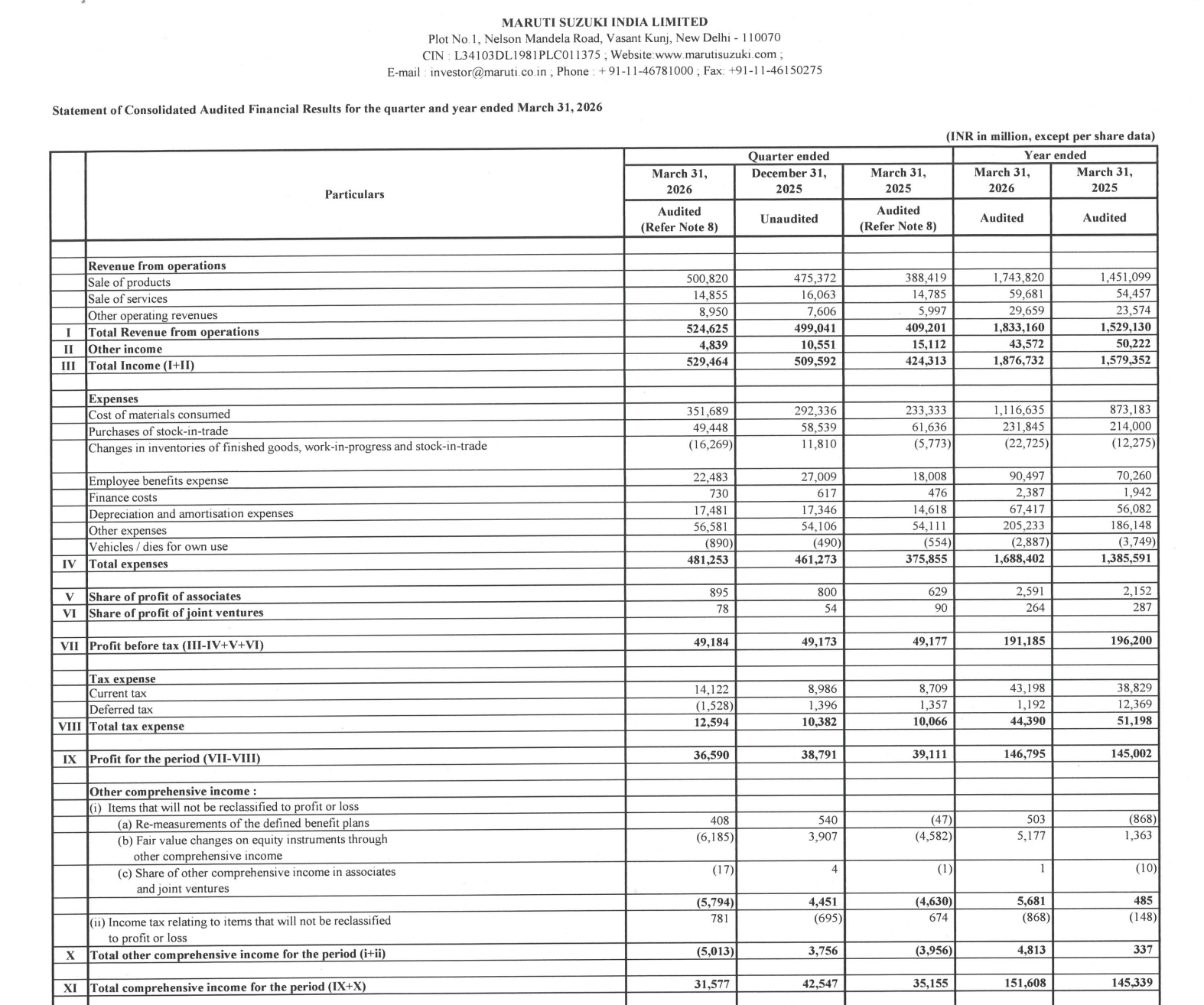

Quarter Ended: March 2026

Maruti Suzuki – Q4 FY26 Results Analysis

NSE

maruti

BSE

532500

Strong volume-led revenue growth continues, but rising input costs and operating expenses have compressed margins and impacted profit growth

key financial highlights

- Revenue from Operations:

- Revenue (Q4 FY26): ₹5,24,625 million

- QoQ Change: +5.1%

- YoY Change: +28.2%

- Previous Quarter (Q3 FY26): ₹4,99,041 million

- Previous Year (Q4 FY25): ₹4,09,201 million

- Revenue (Q4 FY26): ₹5,24,625 million

- Profit After Tax (PAT):

- PAT (Q4 FY26): ₹36,590 million

- QoQ Change: -5.7%

- YoY Change: -6.4%

- Previous Quarter (Q3 FY26): ₹38,791 million

- Previous Year (Q4 FY25): ₹39,111 million

- PAT (Q4 FY26): ₹36,590 million

- QoQ Performance

- Revenue Trend: Moderate growth

- Profit Trend: Decline

Margin Analysis

Key Drivers:

- Sharp increase in cost of materials (₹351,689 mn)

- Higher employee benefit expenses

- Rising other operating expenses (₹56,581 mn)

- Inventory adjustments impacting cost structure

Key Signal: Despite strong revenue growth, operating leverage is not translating into profit growth, indicating margin compression

Earning quality check

Drivers:

- Strong operating cash flow: ₹190,999 million

- High depreciation (₹67,417 million annually)

- Stable finance costs (₹2,387 million annually)

- Contribution from associates and joint ventures

Interpretation:

- Earnings are high-quality and cash-backed, but margin compression reduces incremental profitability

balance sheet Analysis

- Total Assets: ₹1,488,810 million

- Total Liabilities: ₹417,247 million

Insight:

- Strong equity base (₹1,071,563 million)

- Low leverage structure

- Increase in working capital (inventory + receivables impact)

key risks

- Rising raw material costs (steel, components)

- Margin pressure due to competitive pricing

- Inventory build-up risk

- Dependence on domestic auto demand cycle

management strategy signals

Focus Area:

- Volume expansion

- Cost optimization

- Product portfolio strengthening

- EV and hybrid transition

Financial Metrics

| Particular | Q4 FY26 | Q.O.Q | Y.O.Y |

|---|---|---|---|

| Total Income | ₹5,29,464 Million | +3.9% | +24.8% |

| PBT | ₹49,184 Million | Flat | +0.01% |

| PAT | ₹36,590 Million | -5.7% | -6.4% |

Maruti Suzuki continues to deliver strong top-line growth driven by demand and scale, but profitability remains under pressure due to rising costs. The company remains fundamentally strong with a robust balance sheet, but near-term margin expansion looks constrained

Official Exchange Filing: Maruti Suzuki Ltd

Quarterly Performance Context

COST OF OPERATIONS AS % OF REVENUE

92%

NET PROFIT AS % OF REVENUE

7%

FISCAL YEAR

2025-2026

AUDIT STATUS

REVIEWED