Quarterly & Annual Financial Results

ONGC Reports 53% Surge in Q4 Consolidated Net Profit; Declares Highest-Ever FY26 Dividend Payout

NSE

ONGC

BSE

500312

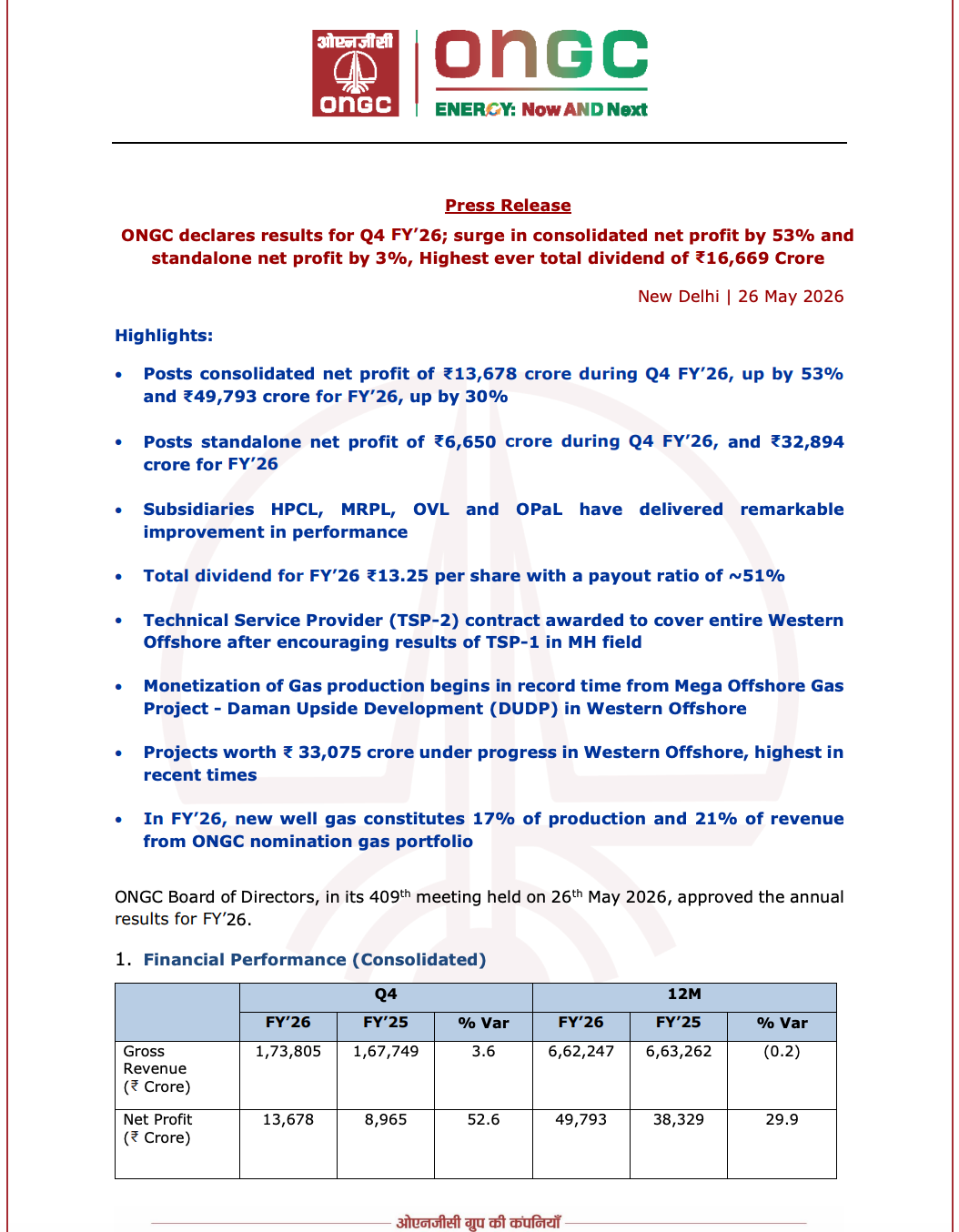

Oil and Natural Gas Corporation (ONGC) reported a strong FY26 performance led by significant improvement in consolidated profitability, recovery in subsidiary earnings, higher gas monetization from new wells, and strategic offshore production initiatives. Consolidated Q4 FY26 net profit rose 53% YoY to ₹13,678 crore, while the company declared its highest-ever annual dividend payout of ₹16,669 crore.

PRICE-SENSITIVE TRIGGER

Event: ONGC announced audited Q4 FY26 and FY26 financial results along with operational, exploration and strategic business updates.

Type: Quarterly & Annual Financial Results

Impact: Positive

Immediate Effect: Strong consolidated earnings growth, record dividend payout, improved subsidiary profitability and progress in offshore gas monetization strengthen ONGC’s operational and financial outlook.

Key Metrics:

- Consolidated Q4 FY26 Gross Revenue: ₹1,73,805 crore | +3.6% YoY

- Consolidated Q4 FY26 Net Profit: ₹13,678 crore | +52.6% YoY

- Consolidated FY26 Net Profit: ₹49,793 crore | +29.9% YoY

- Standalone Q4 FY26 Revenue: ₹35,927 crore | +2.7% YoY

- Standalone Q4 FY26 PAT: ₹6,650 crore | +3.1% YoY

- Standalone FY26 Revenue: ₹1,32,509 crore | -3.9% YoY

- Standalone FY26 PAT: ₹32,894 crore | -7.6% YoY

- FY26 Total Dividend: ₹13.25 per share

- Total Dividend Payout: ₹16,669 crore

- Dividend Payout Ratio: ~51%

- New Well Gas Revenue FY26: ₹6,678 crore

- Additional Revenue from New Well Gas: ₹1,223 crore over APM pricing

- Projects Under Execution in Western Offshore: ₹33,075 crore

- Reserve Replacement Ratio (2P): 1.17

- ONGC Group Reserve Accretion FY26: 99.17 MMToE vs 34.46 MMToE in FY25

- OPaL FY26 EBITDA: ₹1,207 crore vs EBITDA loss of ₹203 crore in FY25

- HPCL FY26 Standalone PAT: ₹17,175 crore vs ₹7,365 crore in FY25

- MRPL FY26 PAT: ₹1,931 crore vs ₹51 crore in FY25

Highlight:

- Label: Consolidated Q4 Profit Growth

- Value: Consolidated Q4 FY26 net profit surged 53% YoY to ₹13,678 crore.

What Happened ?

ONGC announced FY26 audited financial results highlighting:

- Strong consolidated profitability growth

- Stable upstream operational performance

- Improved subsidiary earnings

- Accelerated offshore project execution

- Higher contribution from premium-priced new well gas production

The company also:

- Recommended final dividend of ₹1 per share

- Took total FY26 dividend to ₹13.25 per share

- Continued large-scale investment in offshore production infrastructure

- Advanced strategic partnerships and renewable energy initiatives

Key operational developments included:

- Monetization of Daman Upside Development Project (DUDP)

- Expansion of technical collaboration with BP in Western Offshore

- Deepwater exploration acceleration under Project DeepX

- Multiple discoveries and reserve additions across offshore and onshore basins

Subsidiaries including HPCL, MRPL, OPaL and ONGC Green delivered substantial operational and financial improvement during FY26.

Key Details

Operational Performance, Exploration

Expansion & Subsidiary Recovery:

- ONGC’s consolidated FY26 net profit increased nearly 30% YoY despite softer crude realization environment.

- New well gas contributed:

- 17% of total gas production

- 21% of nomination gas revenue portfolio

- DUDP offshore gas project commenced monetization in record time and is expected to increase gas output materially.

- Mumbai High revival program showed early operational success after onboarding BP as technical service provider:

- Oil production reached 102% of target baseline

- Gas production reached 108% of target baseline

- ONGC plans to extend BP-led technical support across the entire Western Offshore region.

- Western Offshore projects worth:

- ₹33,075 crore

are currently under execution, representing one of ONGC’s largest recent offshore capex cycles.

- ₹33,075 crore

- Exploration activity accelerated sharply under Project DeepX:

- Deepwater drilling efforts to double over next two years

- Ultra-deepwater exploratory drilling initiated in Andaman Basin

- Extensive 2D and 3D seismic acquisition conducted in Mahanadi Basin

- ONGC reported:

- 3 hydrocarbon discoveries during FY26

- 3 monetized discoveries during FY26

- Reserve accretion improved significantly:

- ONGC Group reserve accretion rose to 99.17 MMToE from 34.46 MMToE in FY25.

- OPaL reported a major turnaround:

- FY26 EBITDA improved to ₹1,207 crore from negative EBITDA in FY25.

- HPCL delivered:

- Highest-ever refinery throughput

- Highest-ever sales volume

- Strong GRM improvement

- MRPL profitability recovered sharply due to stronger refining margins and operational stability.

- ONGC Green and renewable subsidiaries expanded renewable energy generation and improved profitability.

Note:

- The FY26 performance reflects ONGC’s strategic transition toward:

- Higher-value gas monetization

- Offshore production revival

- Deepwater exploration expansion

- Integrated energy and renewable diversification

- Improved subsidiary capital efficiency

Risk Analysis

Summary:

- Despite strong profitability and strategic progress, ONGC remains exposed to commodity price volatility, geopolitical disruptions, offshore execution risks and production stability challenges.

Key Risks:

- Crude oil realization declined materially on a full-year basis despite Q4 recovery.

- Offshore production remains vulnerable to:

- Reservoir complexity

- Pipeline replacement delays

- Technical shutdowns

- Weather-related disruptions

- West Asia geopolitical issues impacted production and execution timelines.

- ONGC Videsh overseas operations remain exposed to:

- Geopolitical instability

- Production disruptions in foreign assets

- Global commodity cycles

- Deepwater exploration carries:

- High capital intensity

- Longer gestation periods

- Exploration uncertainty

- Refining subsidiaries remain sensitive to:

- GRM fluctuations

- Global energy demand

- Fuel pricing dynamics

- Renewable and transition investments may require sustained capex before meaningful returns scale up.

Worst Case Scenario:

- A sharp decline in crude prices, delays in offshore project execution, weaker refining margins or production disruptions across key offshore assets could pressure earnings growth and cash flow generation.

Risk Level: Medium

Company Commentary

- ONGC stated that:

- Subsidiaries HPCL, MRPL, OVL and OPaL delivered remarkable improvement in performance.

- Management highlighted:

- New well gas now contributes over 21% of nomination gas revenue portfolio.

- ONGC emphasized:

- Projects worth ₹33,075 crore are under progress in Western Offshore to support future production growth.

- The company stated:

- BP’s technical collaboration in Mumbai High has shown encouraging production revival trends.

- ONGC confirmed:

- Deepwater exploration efforts under Project DeepX are being accelerated to unlock long-term hydrocarbon potential.

- Management indicated:

- Renewable energy expansion, energy logistics partnerships and petrochemical restructuring remain strategic priorities for future growth.

Official Exchange Filing: ONGC Limited