Quarterly & Annual Financial Results

Transrail Lighting Delivers Strong FY26 Performance with 30% Revenue Growth and Record Order Book

NSE

TRANSRAILL

BSE

544317

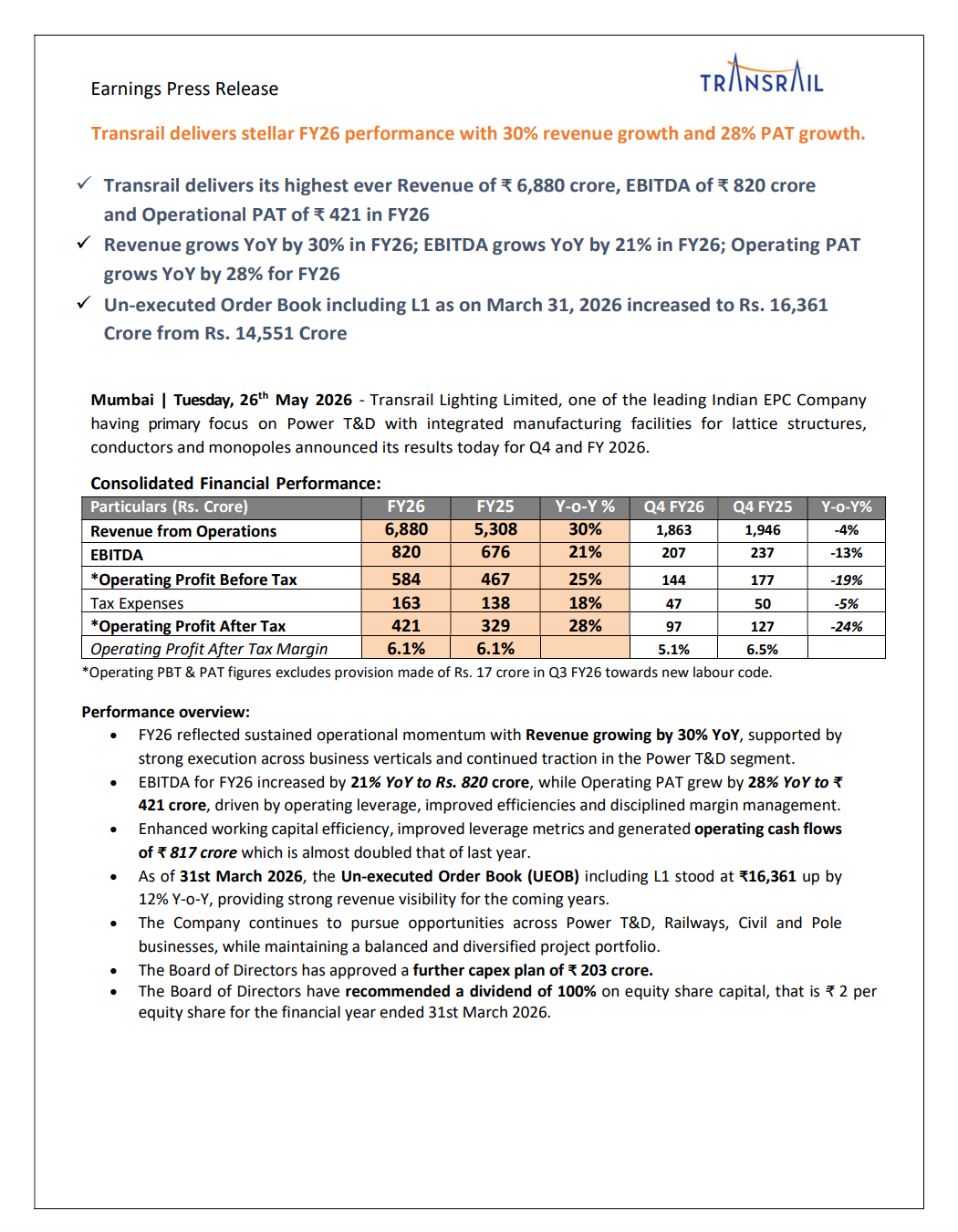

Transrail Lighting Limited reported its highest-ever FY26 revenue, EBITDA and operational PAT, driven by strong execution across Power T&D, Railways and Civil EPC businesses. FY26 revenue grew 30% YoY to ₹6,880 crore, while operational PAT increased 28% YoY to ₹421 crore. The company also reported a record unexecuted order book of ₹16,361 crore and announced additional capex expansion plans.

PRICE-SENSITIVE TRIGGER

Event: Transrail Lighting announced audited Q4 FY26 and FY26 financial results along with operational updates and expansion plans.

Type: Quarterly & Annual Financial Results

Impact: Positive

Immediate Effect: Strong full-year earnings growth, healthy operating cash flow generation, expansion in manufacturing capacity and a growing order backlog improve medium-term revenue visibility and execution confidence.

Key Metrics:

- FY26 Revenue from Operations: ₹6,880 crore | +30% YoY

- FY26 EBITDA: ₹820 crore | +21% YoY

- FY26 Operating PBT: ₹584 crore | +25% YoY

- FY26 Operating PAT: ₹421 crore | +28% YoY

- FY26 Operating PAT Margin: 6.1%

- Q4 FY26 Revenue: ₹1,863 crore | -4% YoY

- Q4 FY26 EBITDA: ₹207 crore | -13% YoY

- Q4 FY26 Operating PBT: ₹144 crore | -19% YoY

- Q4 FY26 Operating PAT: ₹97 crore | -24% YoY

- Q4 FY26 Operating PAT Margin: 5.1%

- Operational Cash Flow FY26: ₹817 crore

- Unexecuted Order Book (including L1): ₹16,361 crore | +12% YoY

- Approved Additional Capex: ₹203 crore

- Recommended Dividend: ₹2 per equity share (100%)

Highlight:

- Label: Record FY26 Revenue

- Value: Transrail reported its highest-ever FY26 revenue of ₹6,880 crore with 30% YoY growth.

What Happened ?

Transrail Lighting announced strong FY26 operational and financial performance supported by:

- Robust execution across Power Transmission & Distribution projects

- Strong order inflows across geographies

- Improved operational efficiency

- Better working capital management

- Capacity expansion initiatives

The company:

- Doubled tower manufacturing capacity during FY26

- Commissioned a new greenfield facility at Butiburi

- Continued conductor capacity expansion plans

- Strengthened leverage metrics and operating cash generation

Despite weaker Q4 profitability due to execution mix and normalization effects, full-year performance remained strong with record revenue, EBITDA and order backlog levels.

The Board also approved:

- Additional capex of ₹203 crore

- Dividend of ₹2 per share for FY26

Key Details

Execution Momentum, Capacity Expansion & Order Book Visibility:

- FY26 revenue growth of 30% YoY was driven by:

- Strong Power T&D execution

- Diversified project portfolio

- Multi-geography order execution

- EBITDA rose 21% YoY to ₹820 crore due to:

- Operating leverage

- Better project execution

- Margin discipline

- Operating PAT increased 28% YoY to ₹421 crore supported by:

- Improved efficiency

- Strong project conversion

- Better cost management

- Operating cash flow generation improved sharply:

- ₹817 crore in FY26

- Nearly double the previous year level

- Unexecuted order book including L1 stood at:

- ₹16,361 crore as of March 31, 2026

- Up 12% YoY

- Provides strong multi-year revenue visibility

- During FY26, the company:

- Doubled tower manufacturing capacity

- Commissioned new Butiburi greenfield plant

- Continued conductor capacity expansion initiatives

- Management indicated sustained opportunities across:

- Power T&D

- Railways

- Civil infrastructure

- Pole businesses

- Additional capex plan of ₹203 crore indicates continued investment toward manufacturing and execution scale-up.

Note:

- While FY26 delivered strong full-year growth, Q4 FY26 profitability moderated YoY due to execution mix normalization and higher comparative base, though management maintained a positive medium-term outlook backed by order visibility and manufacturing expansion.

Risk Analysis

Summary:

- Transrail remains exposed to EPC execution risks, commodity inflation, project timing variability and margin sensitivity in large infrastructure contracts.

Key Risks:

- Q4 FY26 profitability declined YoY despite strong annual growth, indicating margin volatility in project execution cycles.

- EPC businesses remain vulnerable to:

- Raw material price fluctuations

- Supply-chain disruptions

- Delayed customer approvals

- Execution timing shifts

- Large order book execution requires:

- Sustained working capital discipline

- Efficient project conversion

- Timely receivable collection

- Capacity expansion projects may temporarily pressure:

- Cash flows

- Utilization metrics

- Near-term operating efficiency

- International project exposure may carry:

- Currency risks

- Political risks

- Execution complexities

Worst Case Scenario:

- Delays in project execution, margin compression in EPC contracts or weaker order inflows could affect profitability, cash generation and return ratios despite a strong order backlog.

Risk Level: Medium

Company Commentary

- MD & CEO Randeep Narang stated FY26 reflected continued growth momentum despite a dynamic operating environment.

- Management highlighted:

- Highest-ever revenue, EBITDA and PAT performance during FY26.

- The company stated strong execution across businesses and geographies helped maintain industry-leading margins.

- Management emphasized:

- Significant progress in working capital efficiency

- Debt reduction

- Strong operating cash flow generation

- Transrail confirmed:

- Tower manufacturing capacity doubled during FY26

- New greenfield plant commissioned at Butiburi

- Conductor expansion remains underway

- Management indicated:

- Healthy order book and bidding pipeline position the company well for medium-to-long-term growth.

Official Exchange Filing: Transrail Lighting Limited