Credit Rating Upgrade

TFCI Credit Rating Upgraded to BWR AA-/Stable by Brickwork Ratings on Improved Asset Quality and Profitability

NSE

tfci

BSE

526650

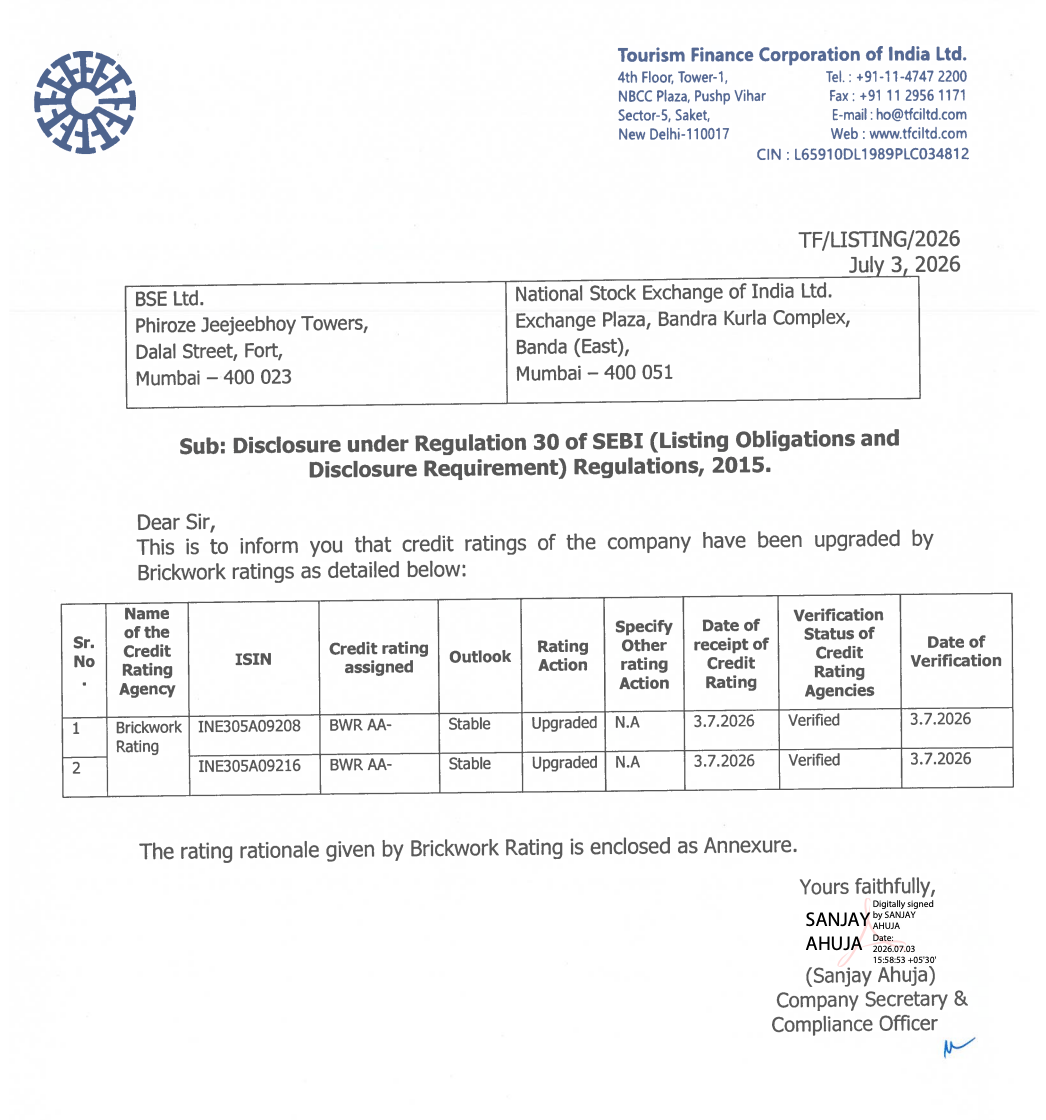

Tourism Finance Corporation of India Ltd. (TFCI) has received an upgrade in its long-term credit rating from BWR A+/Stable to BWR AA-/Stable from Brickwork Ratings for its outstanding non-convertible debentures aggregating ₹175 crore. The upgrade reflects stronger asset quality, robust loan book growth, improved profitability, healthy capitalization, and adequate liquidity.

PRICE-SENSITIVE TRIGGER

Event: Brickwork Ratings upgraded TFCI’s long-term credit rating for its outstanding Non-Convertible Debentures (NCDs).

Type: Credit Rating Upgrade

Impact: Positive

Immediate Effect: The upgraded rating strengthens TFCI’s credit profile, enhances market confidence, and could improve the company’s ability to access debt capital at competitive borrowing costs.

Key Metrics:

- Credit Rating: Upgraded from BWR A+/Stable to BWR AA-/Stable

- Outstanding Rated Bonds: ₹175 crore

- Assets Under Management (AUM): ₹2,088.14 crore (+23.9% YoY)

- Total Income: ₹276.83 crore (FY26) vs ₹260.06 crore (FY25)

- PAT: ₹123.46 crore (FY26) vs ₹103.81 crore (FY25) (+18.9% YoY)

- Net Profit Margin: Approximately 45%

- Gross NPA: Improved to 0.37% from 3.22%

- Net NPA: Reduced to 0.00% from 1.61%

- Net Interest Margin (NIM): Improved to 6.43% from 5.07%

- Capital Adequacy Ratio (CRAR): 55.53%

- Tangible Net Worth: ₹1,304.84 crore

- Liquidity Coverage Ratio (LCR): 258%

- Overall Gearing: 0.83x

Highlight:

- Rating Upgrade Driven By: Significant improvement in asset quality, sustained profitability, diversified loan portfolio, and strong capitalization supported the upgrade to BWR AA-/Stable.

What Happened ?

Tourism Finance Corporation of India Ltd. informed the stock exchanges that Brickwork Ratings has upgraded the company’s long-term rating on its outstanding ₹175 crore Non-Convertible Debentures to BWR AA-/Stable.

The rating agency cited multiple operational improvements during FY26, including strong growth in the loan book, substantial recoveries from stressed assets, lower NPAs, improved profitability, higher net interest margins, and continued balance sheet strength.

Brickwork also noted that TFCI has successfully diversified its lending portfolio beyond tourism and hospitality into manufacturing, real estate, NBFCs, social infrastructure and other resilient sectors, reducing concentration risk while maintaining healthy capital buffers and liquidity.

Key Details

Key Rating Drivers:

- Assets Under Management expanded nearly 24% to ₹2,088.14 crore.

- Gross NPA reduced sharply from 3.22% to 0.37%.

- Net NPA declined to Nil, supported by recoveries of approximately ₹50.35 crore.

- PAT increased nearly 19% to ₹123.46 crore.

- Net Interest Margin improved from 5.07% to 6.43%.

- Loan portfolio diversified beyond tourism into manufacturing, real estate, NBFCs, social infrastructure and loan against securities.

- Tourism sector exposure reduced from 63% to 52%, lowering concentration risk.

- Capital adequacy remained significantly above regulatory requirements at 55.53%.

- Liquidity remained comfortable with cash, liquid investments and LCR well above regulatory norms.

- Brickwork maintained a Stable Outlook, expecting continued improvement in operations and credit profile.

Note:

- The rating upgrade reflects an improvement in TFCI’s standalone credit profile. It does not alter the company’s capital structure or business operations but enhances its credibility in the debt market.

Risk Analysis

Summary:

- While TFCI’s financial profile has strengthened materially, the company remains exposed to sector-specific lending risks, execution risks in financed projects, and the need to sustain current asset quality as its loan portfolio expands.

Key Risks:

- Slippages in one or two large borrower accounts could materially increase NPAs due to the relatively concentrated loan book.

- Tourism and hospitality financing remains sensitive to economic cycles and project execution.

- Maintaining improved Net Interest Margins during rapid loan growth will remain critical.

- Continued diversification is necessary to reduce concentration risk.

- Future rating improvements depend on sustained profitability, asset quality and expansion in AUM.

Worst Case:

- A deterioration in asset quality, GNPA exceeding rating thresholds, slower recoveries, or a significant decline in profitability and capitalization could result in rating pressure.

Risk Level: Medium

Company Commentary

- Brickwork Ratings upgraded TFCI’s outstanding NCD rating to BWR AA-/Stable.

- The upgrade reflects stronger earnings, improved asset quality and diversified lending operations.

- The company maintained healthy capitalization with CRAR above 55%.

- Liquidity remains adequate to meet debt servicing obligations.

- The Stable Outlook indicates a low probability of rating revision in the near to medium term, provided current performance trends continue.

Official Exchange Filing: Tourism Finance Corporation of India Limited