Quarterly Results

Elecon Engineering Reports Q1 FY27 Results with Revenue Growth and Strong Order Book

NSE

ELECON

BSE

505700

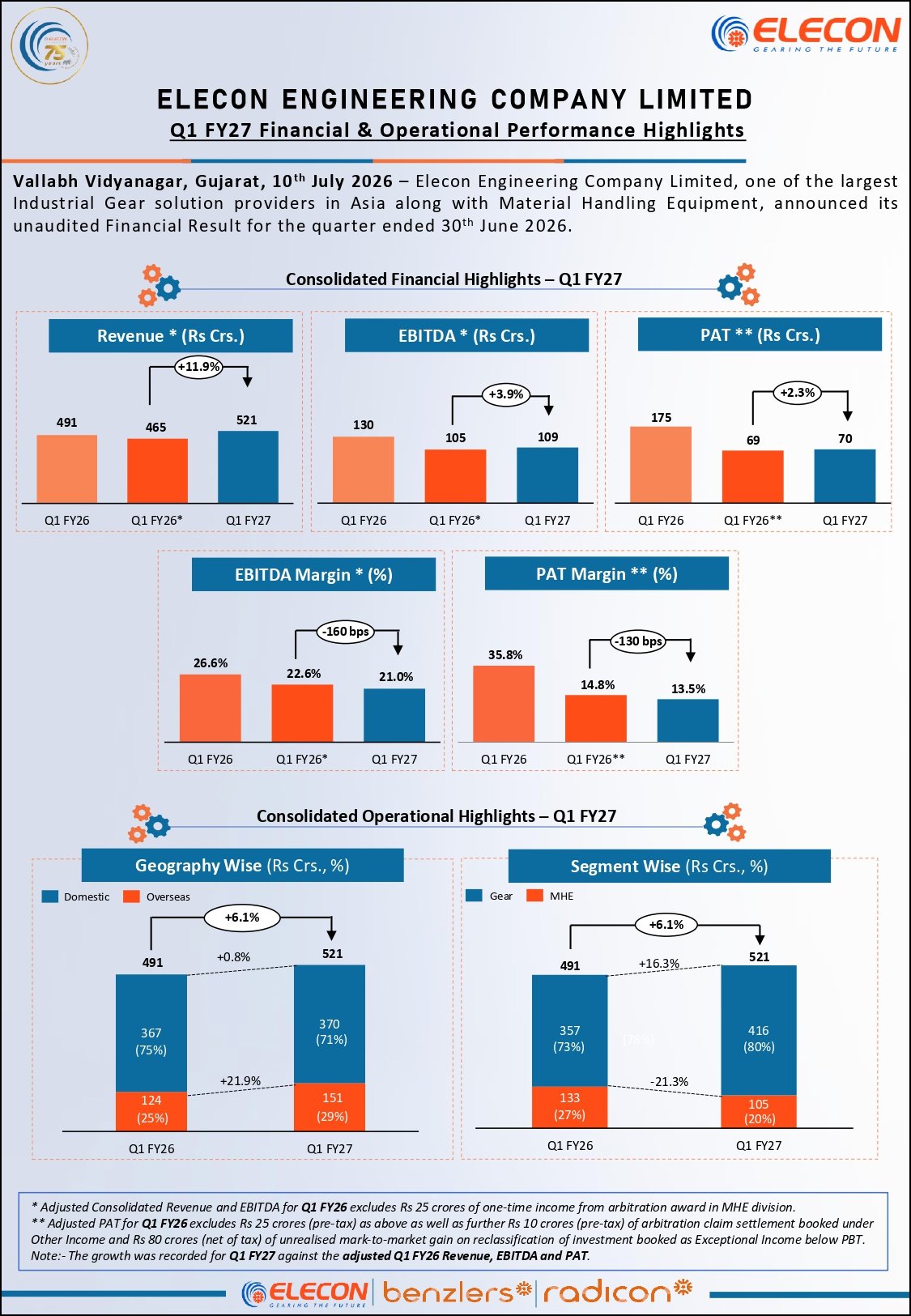

Elecon Engineering reported consolidated Q1 FY27 revenue of ₹521 crore, up 11.9% (adjusted), while EBITDA and PAT grew to ₹109 crore and ₹70 crore, respectively. The company also reported a consolidated order intake of ₹755 crore and an order book of ₹1,518 crore.

PRICE-SENSITIVE TRIGGER

Event: Announcement of Q1 FY27 financial and operational performance.

Type: Quarterly Results

Impact: Positive

Immediate Effect: Elecon Engineering reported 11.9% adjusted revenue growth, 3.9% EBITDA growth, and 2.3% PAT growth in Q1 FY27, supported by strong performance in its Gear Division and a healthy consolidated order book of ₹1,518 crore, providing strong revenue visibility.

Financials:

Key Metrics:

- Gear Division Revenue: ₹416 crore (+16.3% YoY)

- Gear Division EBIT: ₹75 crore (+14.7% YoY)

- Gear Order Intake: ₹570 crore (+18.8%)

- Gear Order Book: ₹1,043 crore (+46.9%)

- Material Handling Equipment (MHE) Revenue: ₹105 crore (-2.9% YoY)

- MHE EBIT: ₹27 crore (-25.3%)

- MHE Order Intake: ₹185 crore (+38.1%)

- MHE Order Book: ₹475 crore (+18.8%)

Highlight:

- Revenue, EBITDA, and PAT increased during the quarter, while the consolidated order book expanded to ₹1,518 crore, driven by robust growth in the Gear Division.

What Happened ?

Elecon Engineering announced its unaudited Q1 FY27 results, reporting higher adjusted revenue and profitability despite margin pressure from increased input costs. The Gear Division delivered strong double-digit growth, while the MHE business experienced temporary softness in execution but continued to build a healthy order pipeline.

Key details

Operational Highlights:

- Consolidated revenue increased to ₹521 crore.

- Overseas revenue grew 21.9% YoY to ₹151 crore, contributing 29% of total revenue.

- Domestic revenue remained broadly stable at ₹370 crore.

- The Gear Division continued to benefit from healthy domestic and export demand.

- The MHE Division secured an overseas Port Industry order worth ₹21 crore during the quarter.

Order Book:

- Consolidated order intake stood at ₹755 crore.

- Consolidated order book reached ₹1,518 crore as of 30 June 2026.

- Management expects the strong order backlog to support revenue growth over the coming quarters.

Risk Analysis

Summary:

- While revenue growth remained healthy, profitability margins moderated due to higher input costs and temporary execution delays in the Material Handling Equipment business.

Key Risks:

- EBITDA and PAT margins declined year-on-year.

- MHE revenue and EBIT remained under pressure.

- Global macroeconomic and geopolitical uncertainties could impact demand.

Worst Case:

- If project execution remains slow and input cost inflation persists, margin recovery and earnings growth could remain subdued in subsequent quarters.

Risk Level: Medium

Company Commentary

- Management stated that the company delivered another quarter of resilient performance, supported by strong execution in the Gear Division, healthy overseas demand, and a record order pipeline. The company remains confident that its expanding order book, global presence, and continued investments in manufacturing and R&D will support sustainable long-term growth.

Official Exchange Filing: Elecon Engineering Limited